Overview

The UK's EV charging sector is at a pivotal inflection point in February 2026, with a surge in mergers and acquisitions highlighting the industry's maturation amid escalating costs, funding pressures, and the push for scale.

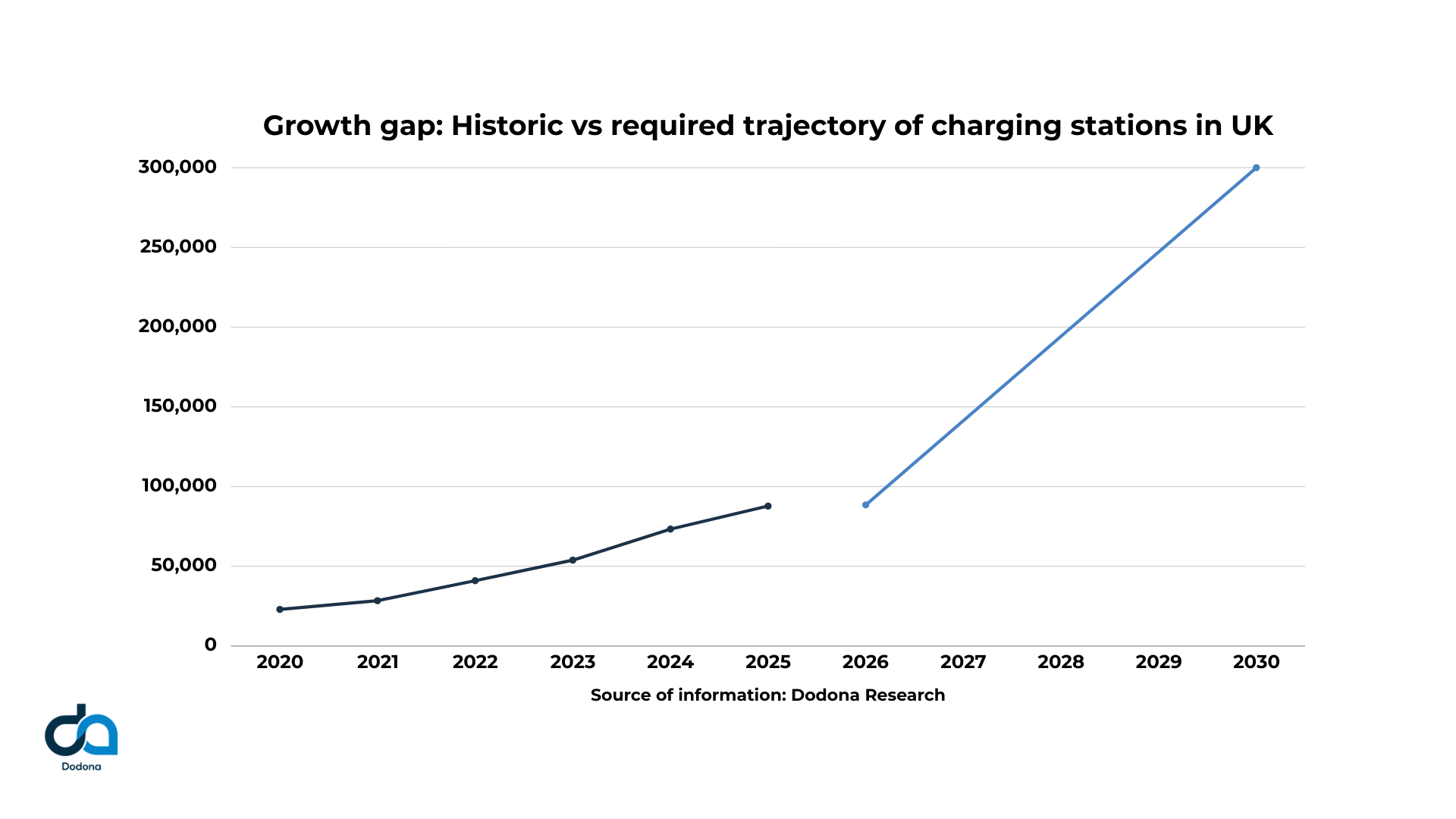

EV sales accounted for 24% of the new-car market in 2025, with plug-in hybrids adding another 20% by year-end, driving unprecedented demand for infrastructure. The network grew 19% in 2025, adding 14,097 new devices to reach 87,796 by year's end, and 88,513 by early 2026. Yet the market remains fragmented, with over 100 operators vying for position. The real question is no longer who the leaders are, that is already clear, but whether 2026 is the year the winners finally self-identify, potentially narrowing the field to a handful of dominant players.

To understand what is at stake, consider the destination: the UK will need between 300,000 and 480,000 public charging points by 2030 to support full EV adoption, compared to today's ~88,500. The gap between now and then is where fortunes will be made and lost. This article explores the key acquisitions driving consolidation, what they reveal about two distinct paths to scale, and how operators can use data-driven decision-making to become winners.

Recent acquisitions

Early 2026 has seen a flurry of deals, particularly in on-street charging, which is crucial for the 52% of potential EV buyers without home charging access. These moves are strategic responses to a market where smaller operators struggle with cash flow and scale.

| Acquisition | Buyer | Seller/Target | Key Details | Type of Deal |

|---|---|---|---|---|

| Be.EV acquires Mer's UK network | Be.EV (backed by Octopus Energy) | Mer (owned by Statkraft) | Adds 1,600+ bays across 450 sites, tripling Be.EV's footprint to over 2,500 bays, focusing on southern England | Proactive: Enhances regional coverage and integrates with energy tech for grid-smart charging |

| Shell-Ubitricity acquires SureCharge | Shell-Ubitricity | SureCharge (from FM Conway) | Integrates 2,400+ lamppost chargers, boosting Ubitricity to >14,400 units across 30+ authorities | Divestiture: FM Conway shed a non-core business, allowing Ubitricity to solidify its lead in on-street AC charging |

| Connected Kerb acquires Trojan Energy | Connected Kerb (backed by National Wealth Fund) | Trojan Energy | Absorbs 1,500 plug-into-the-pavement sockets and innovative Flat & Flush tech after Trojan's funding shortfall | Distressed: Trojan entered administration on February 9, 2026, due to inability to secure growth funding; pre-pack sale saved 63 jobs and preserved operations |

| PLUG Charging acquires Wattif EV UK | Plug Charging | Wattif EV UK | Adding 350 plugs to their growing network | Proactive: All sites fully integrated into the Plug Charging operational platform |

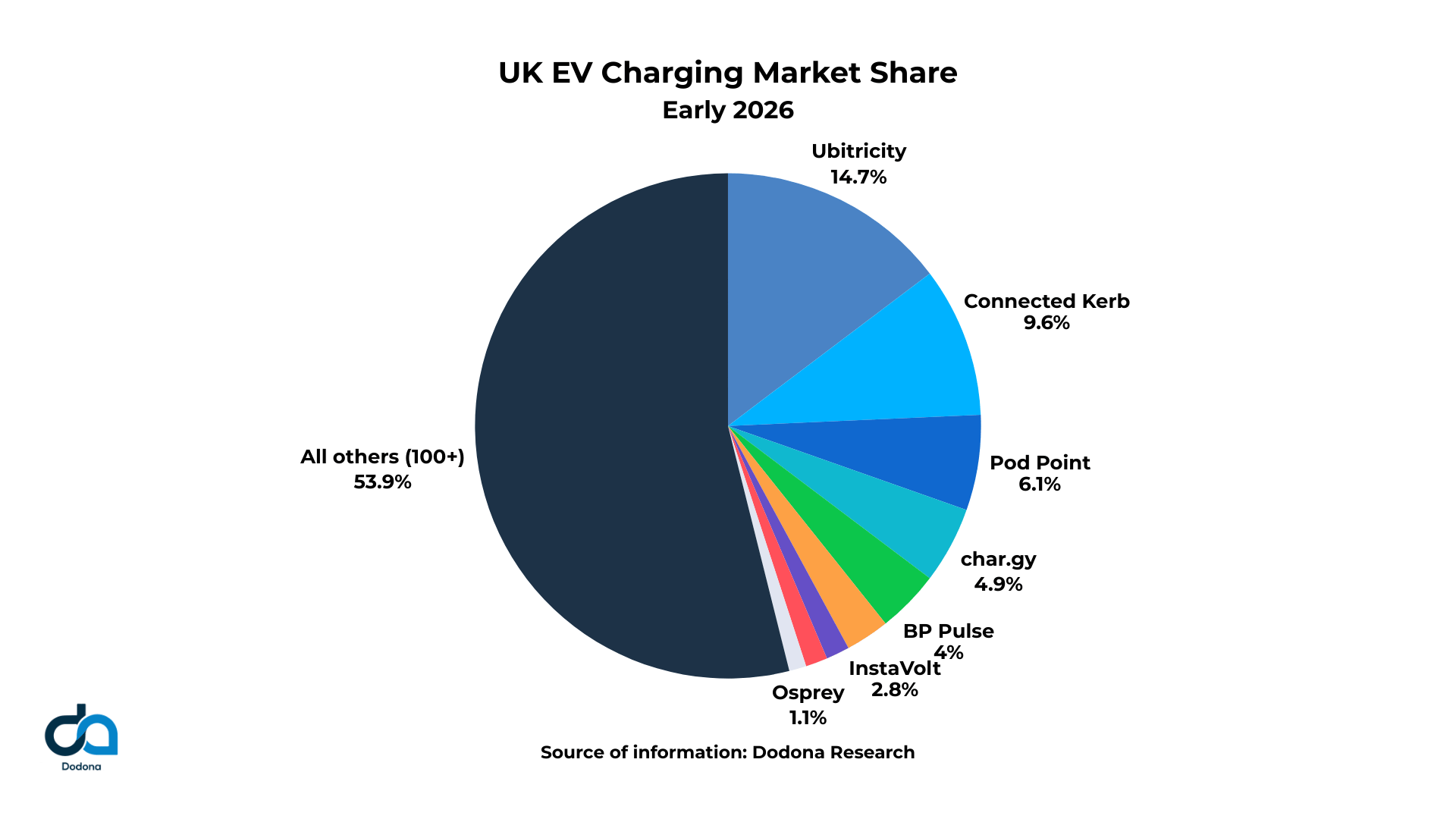

These acquisitions have propelled Ubitricity and Connected Kerb to the forefront of on-street providers, with Ubitricity now at >14,400 chargers (mostly AC lampposts) and Connected Kerb at ~8,500 (post-Trojan). The top 10 operators already control 54% of all UK charge points.

Two paths to scale

The deals reveal two distinct M&A archetypes:

Distressed Sales (e.g., Trojan Energy): Trojan's administration filing on February 9, 2026, stemmed from funding hurdles despite deploying 1,500 sockets. This bargain-hunting approach allows buyers like Connected Kerb to acquire undervalued assets quickly through pre-pack administration, integrating technologies such as Trojan's subsurface chargers that minimise street clutter. But distressed acquisitions demand rigorous due diligence: if a network was not profitable for one operator, what makes it viable for the next? In Trojan's case, only 700 of 1,500 sockets met premium criteria for reliability and demand, a judgment that requires assessing locations, hardware state, and commercial potential before committing capital.

Proactive Investments (e.g., SureCharge, Mer): These include divesting non-core assets (e.g., SureCharge from FM Conway) or pursuing strategic expansions (e.g., Be.EV-Mer). Buyers gain immediate scale, as seen with Ubitricity's jump to market leader status, enabling nationwide contracts and stronger supplier negotiations.

As Be.EV's Asif Ghafoor has noted that many operators are cash-strapped and seeking exits, predicting further M&A. This trend aligns with the Zero Emission Vehicle (ZEV) mandate, targeting 29% EV sales in 2026.

Why fragmentation won't last: Two views

The UK has ~88,513 public chargers, but the market is long-tailed: the top three on-street players (Ubitricity, Connected Kerb, chargy) control ~50% of AC chargers, with the remaining 50% spread across 20+ smaller operators, resulting in inefficient nationwide operations. Scale is essential to viability, as echoed by Connected Kerb's CEO Chris Pateman-Jones: the CPO model only works at critical mass. Imagine field engineers servicing 300 scattered chargers from Aberdeen to Cornwall, costs skyrocket without density. Smaller firms might survive with hyper-local strategies (e.g., dominating Birmingham), but national ambitions demand consolidation.

Yet the path to that consolidation is hotly debated, even within Dodona. Will EV charging follow the trajectory of oil and gas, consolidating into a handful of dominant players through M&A? Or will it remain fragmented, like the US utilities market, where over 3,200 providers still coexist?

Chris Chamberlain, Head of Sales: The consolidation case.

I personally think it will consolidate to a much higher degree than remain fragmented. EV charging is fundamentally different from utilities. With utilities, you don't really interface with your provider; you turn your lights on, and they work. But with EV charging, you're a public-facing brand where businesses or individuals have a direct relationship with that provider. You need to interact, understand the nuances, apps, interoperability, and reliability. That consumer-facing relationship creates stronger economies of scale, making consolidation inevitable. We'll see a handful of dominant national players emerge, with the middle ground, too big to be local, too small to be national, getting squeezed out entirely.

Stefan Furlan, CEO: The niche opportunity case.

I see it slightly differently; perhaps consolidation won't happen as quickly. There are enormous specific opportunities for niche players across this market. Yes, you have companies like Ubitricity that work within Shell, which covers a wide range of charging scenarios. But on the other hand, you have very focused niche players who can be extremely successful. Connected Kerb started as a residential on-street charging specialist. Be.EV focused intensely on the Greater Manchester niche and built an incredible local brand with superior service and pricing before expanding to the broader UK. Then you have destination charging deals: McDonald's, Lidl partnering with specific CPOs, where a retailer with 1,000 locations creates a ready-made network. Fleet charging is another entirely distinct niche with its own dynamics and economics, where if your vehicles can't charge, you're literally losing money every hour. The market is large and diverse enough to sustain specialists alongside the giants.

The likely outcome: Both are partly right. We'll see a hybrid market, a small number of dominant national players alongside durable niche specialists, with the middle ground, those too big to be local and too small to be national, being the most exposed to acquisition or exit pressure.

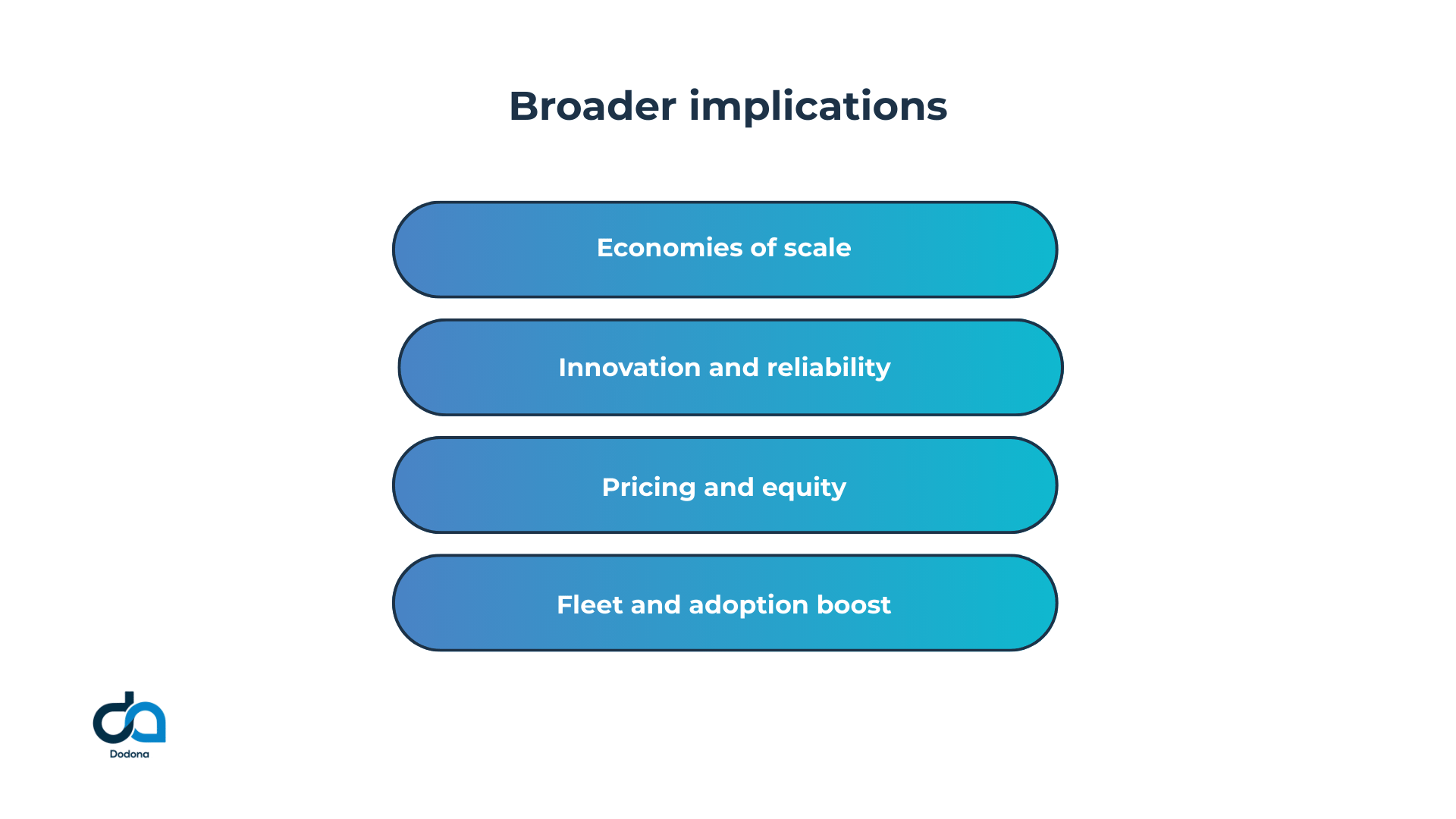

Broader implications

Economies of scale

Merged entities reduce costs through bulk purchasing and streamline operations, accelerating ultra-fast rollouts (e.g., BP Pulse's goal of 3,000 rapid units). The market, valued at USD 518M in 2026 and projected to reach USD 939M by 2031, benefits.

Innovation and reliability

Deals like Trojan's bring pavement-integrated tech, advancing interoperability (OCPP 2.0.1) and Vehicle-to-Grid (V2G) for grid stability amid £2.7B balancing costs.

Pricing and equity

Fewer players may stabilize prices, but public charging (up to 7p/mile post-2026 tax) risks a two-tier system. Fossil giants' involvement (Shell, BP) sparks greenwashing debates.

Fleet and adoption boost

With £1.3B in extended grants and £100M in infrastructure funding, acquisitions support fleets through multi-hub sites and Charging-as-a-Service (CaaS).

Challenges include grid upgrades, new pay-per-mile taxes that could curb demand, and utilization bottlenecks (charging sessions up 34% in 2025, outpacing installations).

How Dodona can help

At Dodona, we're proud to support the charge point operators leading this consolidation wave: Connected Kerb, Ubitricity, Be.EV, and Plug Charge are all Dodona clients, using our platform to drive smarter investment and expansion decisions. And it is no coincidence that our clients are the operators who have been successful enough to make acquisitions in the first place.

We help leading charge point operators and investors turn today's consolidation wave into an opportunity to build profitable networks at scale. Our platform brings together 50+ data sources, AI automation, and intuitive workflows to answer three critical questions for any acquisition or portfolio decision:

-

Could you deploy?

-

Should you invest?

-

And where do you start?

Our clients already see 110% network growth vs a 52% industry average and identify nearly three times as many feasible sites as the market.

As 2026 defines the next generation of UK EV charging leaders, the winners will be those who pair consolidation with intelligent, data-driven planning.

If you are evaluating acquisitions or need to optimise your existing network, Dodona can help you find the right sites, invest with confidence, and prioritise the rollout that fits your strategy.

Get in touch to see how our platform can support your next move and to schedule a free demo.