Network Growth vs 52% Industry Average

Site Feasibility vs 30% Market Average

Planned Infrastructure Investment by 2030

Trusted by industry leaders

No More Guesswork

With over fifty data sources, our platform rapidly identifies relevant locations in a single simple screen, putting all the feasible sites at your fingertips.

Should you invest?

Just because you can, should you? With a few clicks, our proprietary AI-driven model provides instant return-on-investment insight so you can confidently invest in viable sites.

Where do you start?

You've identified the opportunity to invest, but which sites do you pick first? Our platform automatically prioritizes the best-performing sites based on your strategy.

vs 52% industry average

vs 30% market average

by 2030

new chargers in 2023

New Research

- 3 business approaches for CPOs

- 8 success factors for EV charger locations

- 10 must-have capabilities in a CPP platform

With over fifty data sources, our platform rapidly identifies relevant locations in a single simple screen, putting all the feasible sites at your fingertips.

AI-Powered

Just because you can, should you? With a few clicks, our proprietary AI-driven model provides instant return-on-investment insight so you can confidently invest in viable sites.

Easy to use

You've identified the opportunity to invest, but which sites do you pick first? Our platform automatically prioritizes the best-performing sites based on your strategy.

Geographic Analysis

Real-time location data

Data Sources

100k+

Locations Analyzed

Visualize how your charging infrastructure will integrate into real-world environments with our advanced modeling capabilities.

Analysis

Assessment

Planning

blog

Latest ideas and updates

European Charging Right Now: What we are seeing in the Netherlands, Germany and Spain

We work with charge point operators across Europe, and one pattern comes up in almost every conversation: the European charging market gets discussed as if it were a single market. It is not. An operator running sites in Rotterdam, Frankfurt and Valencia is running three different businesses with three different constraints, and the strategy that works in one will fail in the other two.

We picked these three countries deliberately. Each one clearly represents a different problem that the whole continent will face at some point. The Netherlands shows what happens when a mature market runs out of grid. Germany shows what a massive, state-driven buildout does to everyone's site economics. Spain illustrates the risks of an early market in which infrastructure outpaces the drivers. Wherever you operate, at least one of these is either your market's future, your current situation, or a phase you have already worked through yourself.

Here is what each one is dealing with in 2026, what they can learn from each other, and where we fit in.

Netherlands: the grid has become the market

The Dutch charging market served as Europe's showcase for a decade. Over 40% of new cars sold in 2025 were electric. The public network passed 200,000 charging points, the densest coverage in the world. Then the grid ran out.

The scale of the problem is hard to overstate. Regional grid operators hold more than 14,000 open requests for offtake capacity, totalling around 9 GW. TenneT's national queue holds a further 38 GW. Stedin has declared parts of the Utrecht network closed to new capacity indefinitely, with no reopening date. Businesses seeking new connections or expansions report waiting up to 10 years. The congestion has now reached households too: Liander placed 7,300 homes on a waiting list this year, some facing three-year delays for a heavier connection, largely driven by heat pumps and home chargers.

The government's response tells you where this is heading. The grid congestion campaign announced in February 2026 contains eight measures, and almost none of them involve building faster. Instead: flexibility tenders from every major grid operator this year, an extra €500 million per year for contracting flexible capacity, subsidies for flexibility scans, and new rules from the consumer authority arriving in July. The official position is explicit: grid capacity will stay scarce in the new energy system, and flexible use of what exists must become standard practice.

For a CPO, this entirely rewrites site selection. In most markets, the question is whether a location has the demand. In the Netherlands, the first question is whether a location can be energised at all, and getting that answer wrong costs years, not weeks. A site with perfect traffic, strong footfall and no grid access is worth nothing. At the same time, locations with available capacity have become the scarcest and most contested assets in the market, and the operator who identifies them first wins them.

Three things follow for anyone operating there. When one of those rare connectable opportunities does surface, the operator who can assess it fastest and with the most conviction takes it. Speed alone is not the whole game, though, because scarcity inflates prices, and a contested asset is exactly the kind you overpay for in the heat of a negotiation. The operators who come out of this period healthy will be the ones who modelled precisely what each site is worth to them and how far they can and will go before the bidding starts, so that conviction arrives with a ceiling built into it. And with expansion constrained, the network you already run becomes the growth engine, which makes it essential to know how each of your sites performs against nearby competitors and, where a site underperforms, whether the cause is low footfall, the wrong charger mix, new competition or something else entirely. Each of those has a different fix, and in a market where you cannot simply build your way out, fixing what you have is the strategy.

Dodona helps you understand how your network is performing and why, so you can optimise based on recent trends.

Germany: nine thousand new fast chargers are about to test everyone's demand assumptions

Germany's problem is the opposite one. The Deutschlandnetz programme plans to deliver around 9,000 high-power charging points across more than 1,000 locations by the end of 2026, each rated at 300 kW or higher, with locations based on a government needs analysis rather than on operator site selection. AFIR adds mandatory fast charging every 60 km on main routes. In May, the Federal Ministry of Transport opened a €1 billion programme for heavy-duty charging, paying €500 per installed kilowatt for depot and public projects. The first funding calls opened on 26 May with a 7 July deadline, and further calls will follow over the programme's four-year term. The Masterplan Ladeinfrastruktur 2030 targets one million public points by the end of the decade.

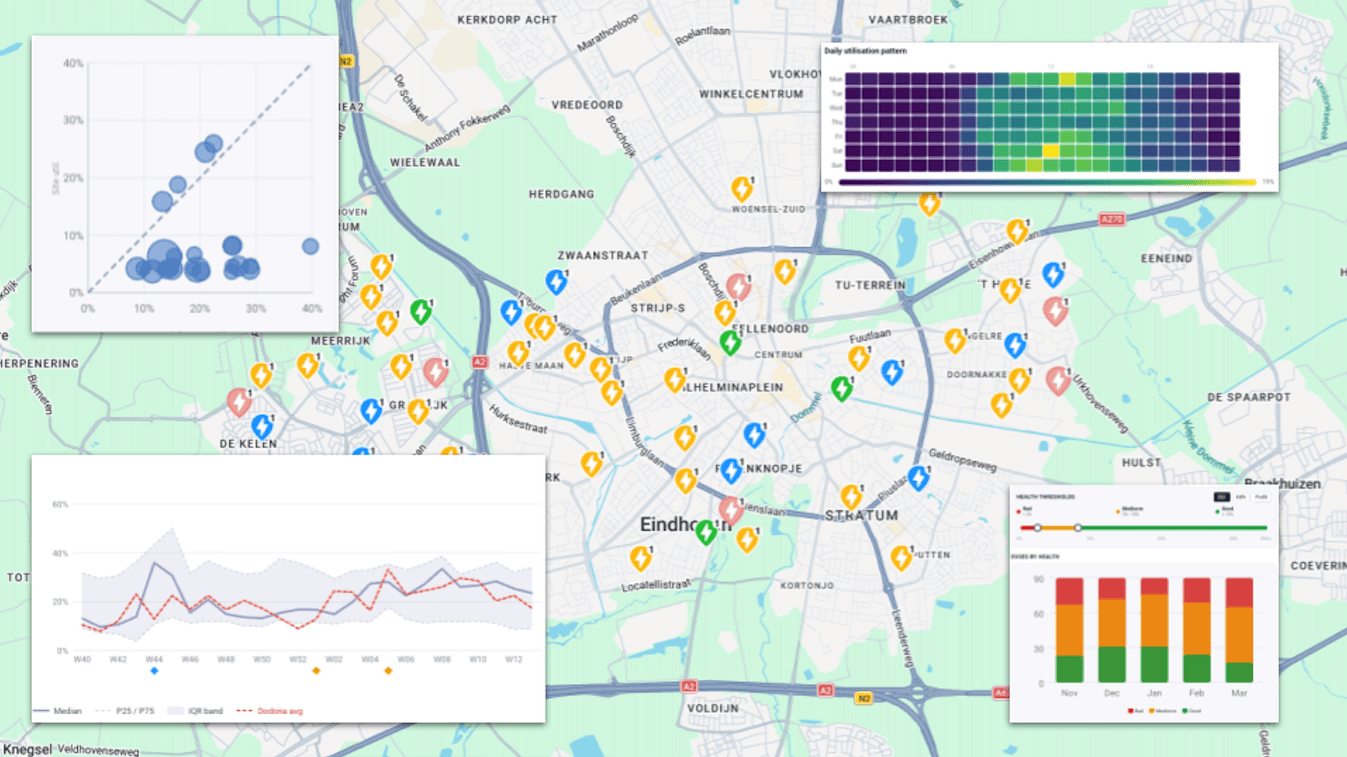

Two consequences follow, and both punish slow analysis. The first is competitive. A site that pencilled last year may not pencil next year once a subsidised 300 kW hub opens a few kilometres away. German operators now need to underwrite every location against a charging map that is redrawing itself monthly, which means knowing exactly where competitors and Deutschlandnetz sites are landing, and what that does to each site's numbers. Commercial sites in Germany need roughly 20-25 sessions per day to cover their tariff structures after accounting for grid costs. Plenty of new capacity will fall short of that, and the difference between winners and casualties will come down to who read the local competitive picture correctly before committing capital.

The second consequence is speed. The funding programmes run on fixed windows and competitive selection, so the operator who can assess a large portfolio in days rather than months gets to bid on more of them, with better numbers. This is exactly the kind of situation Dodona was built for. Operators import candidate sites in bulk, and the platform scores each site against traffic, competition, demographics, and dozens of other data layers, delivering ranked results in minutes. One team used it to evaluate 238 locations over a weekend and submit a competitive tender by Monday morning. When funding rounds have deadlines and the competitive map changes monthly, that turnaround is not a convenience. It determines how much of the German buildout you can participate in.

To illustrate the impact competitors have on a portfolio you are assessing, we conducted a case study. The following are 4 snapshots from our platform showing an example portfolio over a 3-month period. The first shows all the sites, and the following shows the number of sites where competition deployed a charger in the vicinity since the beginning of observation.

Spain: the chargers exist, the demand map does not

Spain's numbers look healthy at a distance. The public network is approaching 50,000 charging points. Corridor operators like Zunder, Repsol and Iberdrola are investing heavily in ultra-fast highway sites; Plenitude plans to achieve full coverage of its Spanish service areas by the end of 2026, and EU money continues to flow through AFIR obligations and EIB financing.

Up close, the picture fractures. AEDIVE reports persistent problems with territorial distribution and administrative activation, meaning a meaningful share of installed chargers sit waiting for grid connection or paperwork, built but not selling a single kilowatt hour. Permitting varies across seventeen autonomous communities, each with its own set of rules, so a project timeline in Madrid tells you nothing about one in Extremadura. Deployment is concentrated in Madrid, Catalonia, and the Basque Country, while other regions barely move. And underneath all of it, electrified vehicles still make up under 2% of the national parc, even as registrations grow at double-digit rates. Spain is building infrastructure ahead of the drivers, which makes every placement decision carry more risk than it would in a mature market.

In a market this thin, intuition fails. The demand that exists is concentrated: around specific corridors, specific urban zones under low-emission pressure, and specific pockets of EV ownership. A charger a few kilometres off that concentration is a stranded asset for years, and Spain already has enough of those. What a Spanish operator needs is a way to see where the real demand signals sit: EV registration density, traffic volumes, points of interest, existing competition and more, before capital is committed and long permitting clocks start running.

Dodona answers that in both directions. Operators can score any candidate location against all the demand signals, and, where no pipeline exists yet, flip to outbound mode: define the criteria that matter, such as traffic thresholds, proximity to specific point-of-interest categories, distance from existing competition, etc., and let the platform generate candidate locations from scratch. And because every score breaks down into the underlying data, an operator can walk a landowner, a municipality, or an internal investment committee through the reasoning live rather than present a black-box recommendation. In a market where permitting runs through seventeen administrations, showing the data tends to move conversations faster than asserting a conclusion.

Dodona allows you to find greenfield locations that are specific to your charging scenario. e.g., on-the-go charging (close to motorways, away from competitors, and convenient to stop), destination charging (looking for convenient 1-2-hour dwell-time locations without competition), or public on-street residential (in residential areas away from competitors).

What each market can learn from the others

The three stories read as separate national problems. When put side by side, they become lessons that travel.

The Netherlands is a warning to Germany and Spain about timing. Grid scarcity did not arrive as a crisis announcement; it crept in behind a success story, and by the time it was undeniable, the queues were a decade long. Operators in markets where connections still feel routine should treat that as a window, not a permanent condition. A grid connection secured today is an asset your competitors may not be able to replicate in five years, and the cost of over-securing capacity now is trivial compared to the cost of queueing for it later.

Germany is a warning about static assumptions. A location assessment is a snapshot, and in a market where subsidised capacity lands by the thousands, snapshots age fast. The lesson carries to Spain's corridors, where several operators are racing to cover the same highways: the site that looks uncontested in this quarter's analysis may have two competitors breaking ground next quarter. Underwriting needs to account for where the market is heading, not just where it stands.

Spain is a reminder that the mature markets have half forgotten: deployment counts are not a business. Chargers waiting on paperwork, chargers placed for coverage optics, chargers a few kilometres off the real demand- all of it shows up eventually as utilisation that never arrives. Dutch and German operators planning their next phase would do well to hold on to the discipline Spain is being forced to learn early, because in every market, the money eventually stops rewarding installation and starts asking about revenue per site.

And one lesson holds everywhere: the operators coming out ahead in all three markets are those who understood each location in precise detail before committing, rather than finding out afterwards.

Where we fit in

Dodona is a charge point planning platform, and the way it helps maps directly onto the three problems above.

When opportunities are scarce and contested, as in the Netherlands, speed and precision on each one matter. Operators can score any candidate location within minutes and see how existing sites perform against nearby competitors, including the diagnostic behind an underperforming site: low footfall, too many chargers relative to demand, or a competitor that opened recently. Each cause points to a different fix.

When the pipeline is large, and the clock is running, as in Germany, operators import sites in bulk and get a ranked list scored against traffic, competition, demographics and dozens of other data layers in minutes instead of weeks, fast enough to fit inside a funding window.

When no pipeline exists yet, as in much of Spain, outbound mode generates candidate locations from the criteria that matter to your business. And wherever a decision needs defending, in front of a landowner, a municipality or an investment committee, every score opens up into the individual data behind it, so the conversation runs on evidence rather than on a black box.

If you operate charging infrastructure in any of these markets and want to see how your pipeline scores against the data, we should talk.

Read More

The cost of a percentage point

We talk to many CPO purchasing teams, and most of them run the same exercise when choosing a platform. A detailed spreadsheet appears: feature-by-feature comparisons, weighted scores, price per site, contract terms. Serious work, done properly.

Almost all of them miss the variable that decides the outcome. Platform price is close to irrelevant. The question that matters is: how much more value does one platform create?

To show the absurdity of just how irrelevant price is, we ran an exercise on how much value a site assessment platform that scores sites in a way that produces just 1% better utilisation.

The answer runs into tens of millions of euros. Here is the maths.

The maths on one percentage point

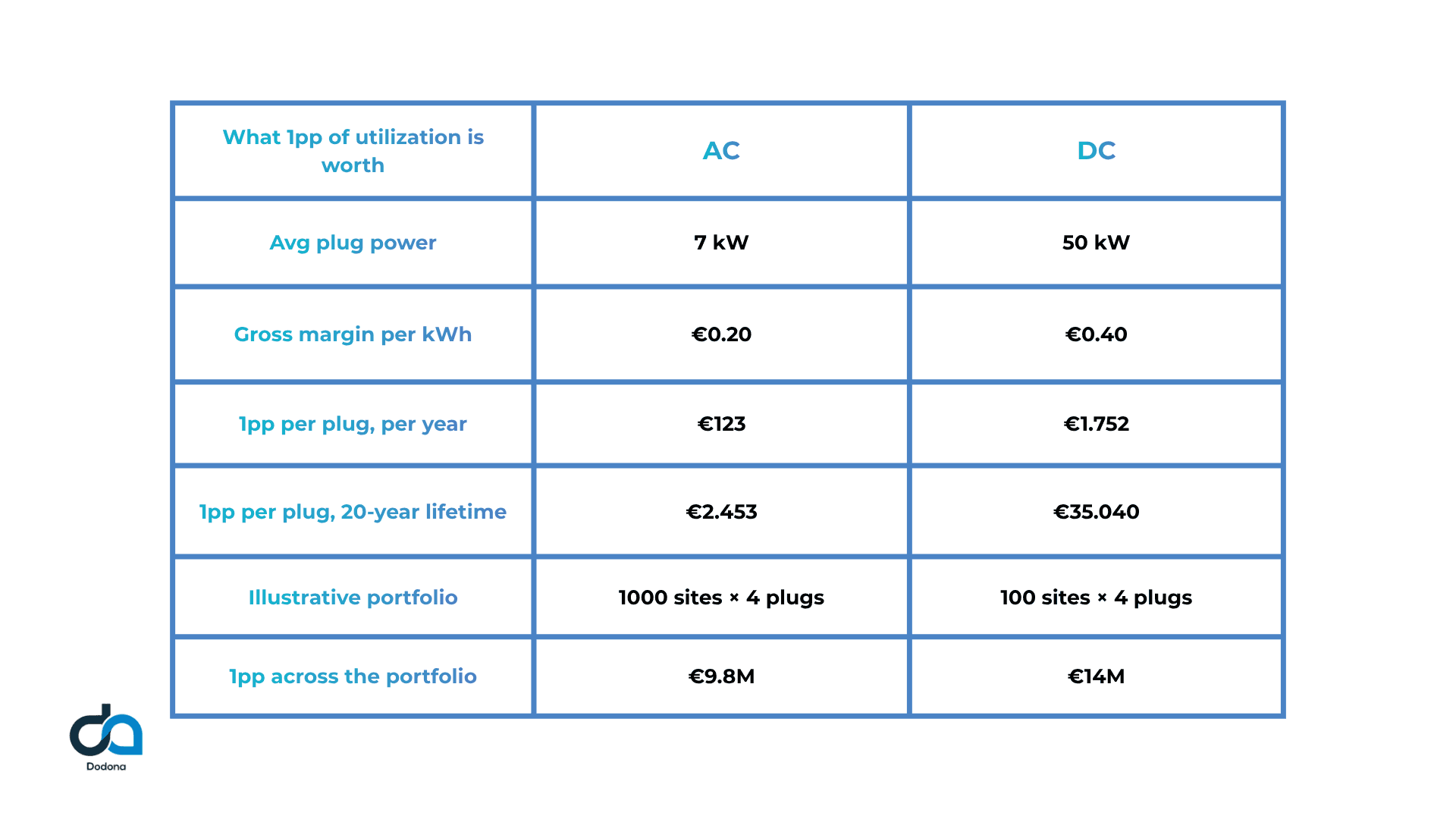

Take illustrative AC and DC portfolios.

A plug runs 8,760 hours a year. At 7 kW delivered power, that is 61,320 kWh per plug at full use. One percentage point of that is 613 kWh per plug, per year. At €0.20 gross margin per kWh, one percentage point is worth €123 per plug, per year. Over a 20-year asset lifetime: €2,453 per plug.

Now scale it. A portfolio of 1,000 locations, with 4 plugs per site, has 4,000 plugs in total. One percentage point of utilisation accuracy across that portfolio is worth €9.8 million over the asset lifetime.

Run the same calculation on DC. A 50 kW plug at €0.40 margin per kWh delivers €1,752 per plug per year for each percentage point, or €35,040 over 20 years. A far smaller portfolio of 100 locations, with 4 plugs each, comes to €14 million.

And 1,000 sites for AC or 100 for DC are modest goals. Most CPOs aim significantly higher, so multiply by 5, 10 or 20 to get to your numbers.

For DC, Fastned, the European fast-charging operator that publishes this number, reported a gross profit per kWh of €0.45 in 2023, rising to €0.58 in early 2026; we use €0.40 to stay on the safe side. For AC, we derived the number as follows: European public AC prices typically range from €0.30 to €0.50 per kWh, compared with commercial electricity costs of roughly €0.15 to €0.25 per kWh, resulting in a gross margin of €0.15 to €0.20 per kWh. We use €0.20, the level a well-run urban AC network reaches. If your numbers differ, substitute them. The shape of the conclusion survives.

The platform price is completely irrelevant

Dodona sits among the pricier solutions in this market. We are fine with that and, honestly, even a bit proud to be the higher-end option. The calculation above explains why the price tag barely matters.

Say the cheaper option saves you a few €10,000s a year but yields results that are 1 percentage point worse. That decision creates a short-term win and costs you in the ballpark of €10 million, even on the modest portfolio above.

That is the entire argument. The shrewd purchase teams we meet reach this conclusion on their own: what a platform costs carries no weight next to how well it lets you assess sites. The gap between a generic benchmark and a model built around a specific portfolio is where the money sits, and we are happy to explain how our site assessment models achieve far better performance there.

So, when you compare solutions, set the price column aside for a moment and ask one question instead: how accurately does each platform let you assess your sites? The answer is worth at least a hundred times the difference between the quotes.

See it on your own numbers

This whole calculation takes twenty minutes with your portfolio inputs. Book a demo. More on how we model utilisation at thedodona.com.

Read More