Resources

Free research!

Aside from our premium content, all of our content is available without you needing to share your contact details.

But if you would like to learn more, see a demo or chat about the value our customers have seen from using our platform, please do not hesitate to get in touch.

case studies

PoGo Charge

PoGo Charge is fast growing UK-wide EV charging network offering ultra-rapid, rapid and destination charging for electric vehicle drivers.

This case study shares how PoGo Charge leverages the Dodona Analytics platform to quickly assess site feasibility and viability to scale its network and the significant benefits this partnership brings to its business. It shares:

- The challenges of scaling a CPO

- The opportunity to move from complex spreadsheets

- 10 solution benefits

Download

FOR EV

FOR EV is a leading provider of EV fleet electrification, working with major clients such as Network Rail Scotland, public bodies, and the private sector.

FOR EV needed complete confidence in its site assessment process, and this case study explores how FOR EV utilizes the Dodona Analytics CPP platform and the benefits this has brought to the business versus their previous process:

- Assessing 500 sites in the time it took to review one

- Focus on good sites with faster site rejection

- Strong reporting and investment readiness

Download

webinars on-demand

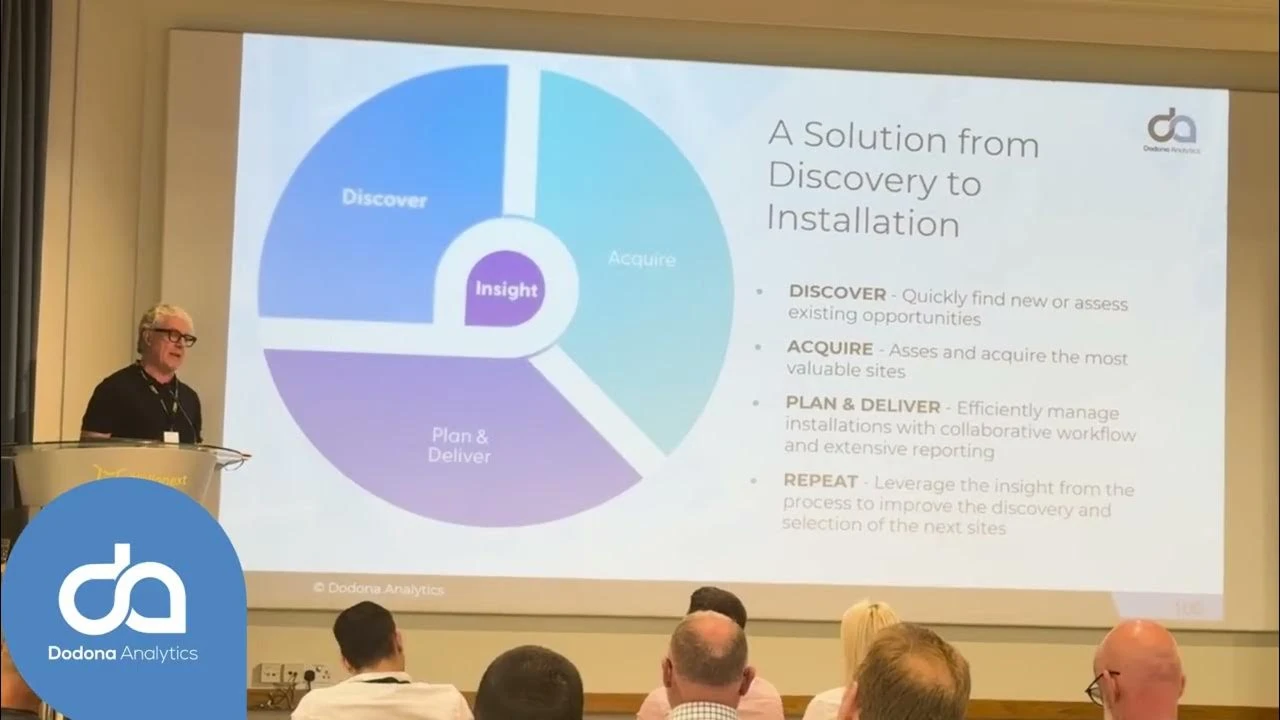

Exploring the Charge Point Planning Market

Industry expert Jeff Clark, Principal Analyst from cleantech insiders joins our co-founder, Chris Chamberlain, to share his latest research into the charge point planning market.

registration required

Watch replay

The Challenge of Happy Chargers

Industry expert Francisco (Paco) Aguirre, Founder, CEO/COO, synergEV joined us for a chat about how to create happy chargers.

registration required

Watch replay

newsletter

Join our community of over 2000 EV experts

Sign up for our monthly newsletter and get the latest EV charging planning tips, news, and insights.

on video

Fireside chat with Stuart Douglas from Pogo Charge

Our friends at Pogo Charge invited our co-founder Chris Chamberlain to have a chat with their MD, Stuart Douglas, to discuss the business of EV charging, how Dodona can help and what they see is the future for EV charging.

Watch on YouTube

Dr Stefan Furlan chats with Asif Ghafoor, CEO, Be.EV

In this conversation, Asif shares the evolution of his business over the last four years working with Dodona, the importance of data analytics in their decision-making, and the innovative approach Be.EV have taken to creating community-focused charging solutions.

Watch on YouTube

Chris Chamberlain speaking at Hellonext's AMPED UP event

Our co-founder, Chris Chamberlain, talks about some of the challenges facing the EV industry and how Dodona Analytics can help at the recent Amped Up industry event.

Watch on YouTube

eBooks

Shareable insight offered free with no need for you to share your contact details.

The Secret Sauce of Successful Charge Point Operators

Explore why Dodona is considered a "secret sauce" and the ingredients that make companies successful in EV charging.

Download

The Business Case For Charge Point Operators

Explore global trends and opportunities for CPOs despite market softening, with insights across UK, US, and EU markets.

Download

The 4 Stages for Success in Site Selection

Four key steps that successful CPOs follow when building commercially profitable charging sites.

Download

Charging Forward with Smart Data

A practical guide to accelerating EV infrastructure and business growth through data-driven decisions.

Download

premium content

The Charge Point Planning Market

- 3 business approaches for CPOs

- 8 success factors for EV charger locations

- 10 must-have capabilities in a CPP platform

This premium content link will take you to a registration page and requires your contact details, which, in accordance with our privacy policy, we do not share.

Download Report

brochures

More information about our product and services to download and share.

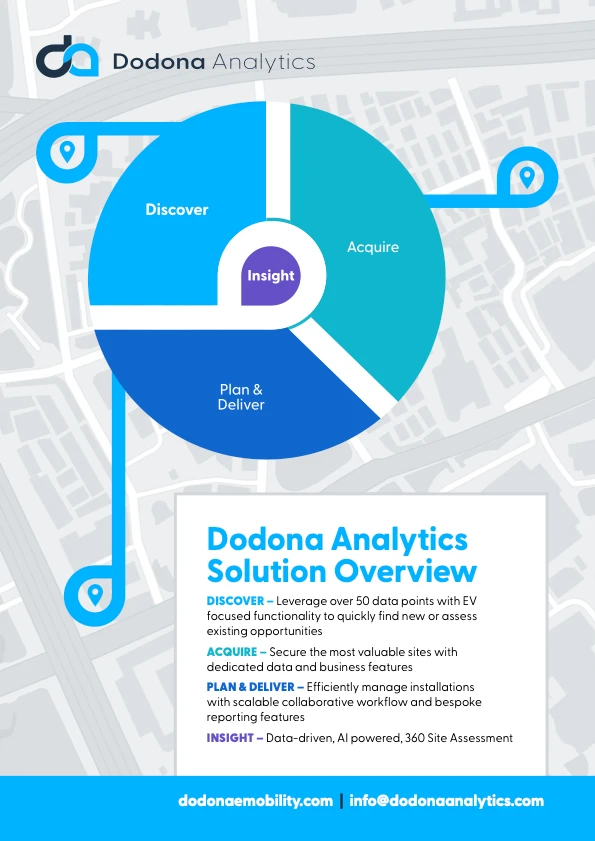

Platform Overview

Get an overview of our platform and how it supports ambitious EV charging planners through the entire process, from discovering new sites, to acquiring them, through the entire planning and delivery process.

Download

Expert Services

Our team has direct hands-on experience working with a wide range of charge point operators, their business models, and specific needs. As such, we have a tried and tested process for organizations new to our platform.

Download

infographic

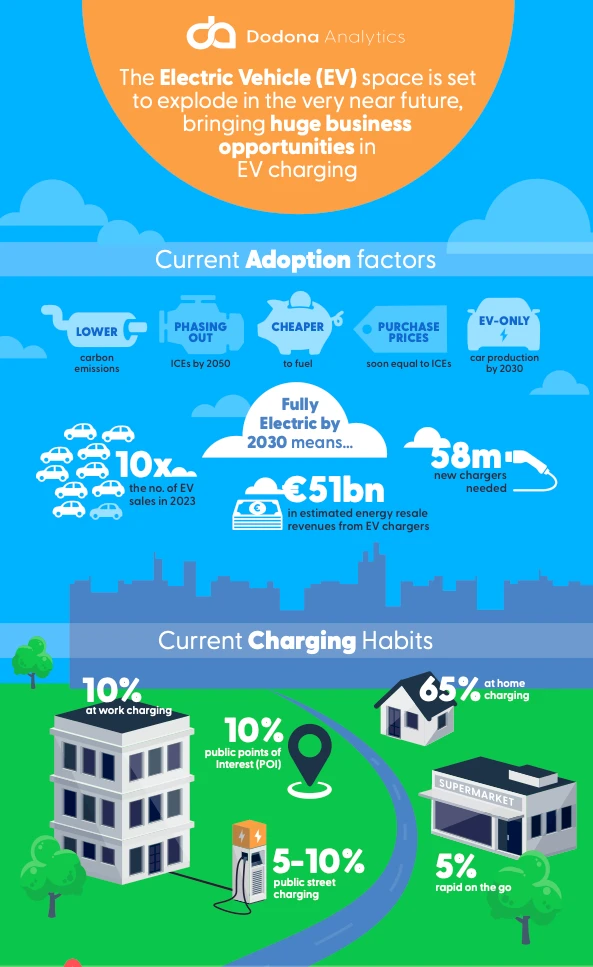

The Emerging EV Charging Landscape

The Electric Vehicle (EV) space is set to explode, bringing huge business opportunities in EV charging. That's according to recent Flashpoint Venture Capital research. We shared the details in this blog post, and we've also created this infographic.

Download Infographic

blog

Deployment was never the hard part

The cheap money that built the charging industry has gone quiet. What comes next rewards a different kind of operator, and it puts fleets at the centre of the story.

The race to deploy left profitability behind

For about three years, building a charging network was mostly a question of speed. Capital was cheap, eager to fund deployment, and the brief from investors rarely changed. Put chargers in the ground, hit the number, and trust that demand will catch up. On paper, the money is still flowing. The appetite behind it has thinned, and the reason matters for anyone planning to rise in the next two years.

The force running the industry now is profitability. Many operators are not making money on the networks they have already built, and everyone can feel the shift. You can see it in who is buying whom. Networks are changing hands across the UK, and the language in every announcement is the same. More scale, a lower cost per site. That is a polite way of describing a route to profit that they could not reach on their own. These are not land grabs. They are the sound of capital running out of patience.

Demand is finally increasing, but not as a rescue

It is worth being clear about how we got here. There was a period of heavy investment built on the assumption that demand would come sooner or later, or at least sooner than it did. Then the last two years emptied the tank. Incentives dried up. The new administration in the United States turned policy back toward oil and rewrote the programmes that had underwritten build-outs. Europe felt the chill, too.

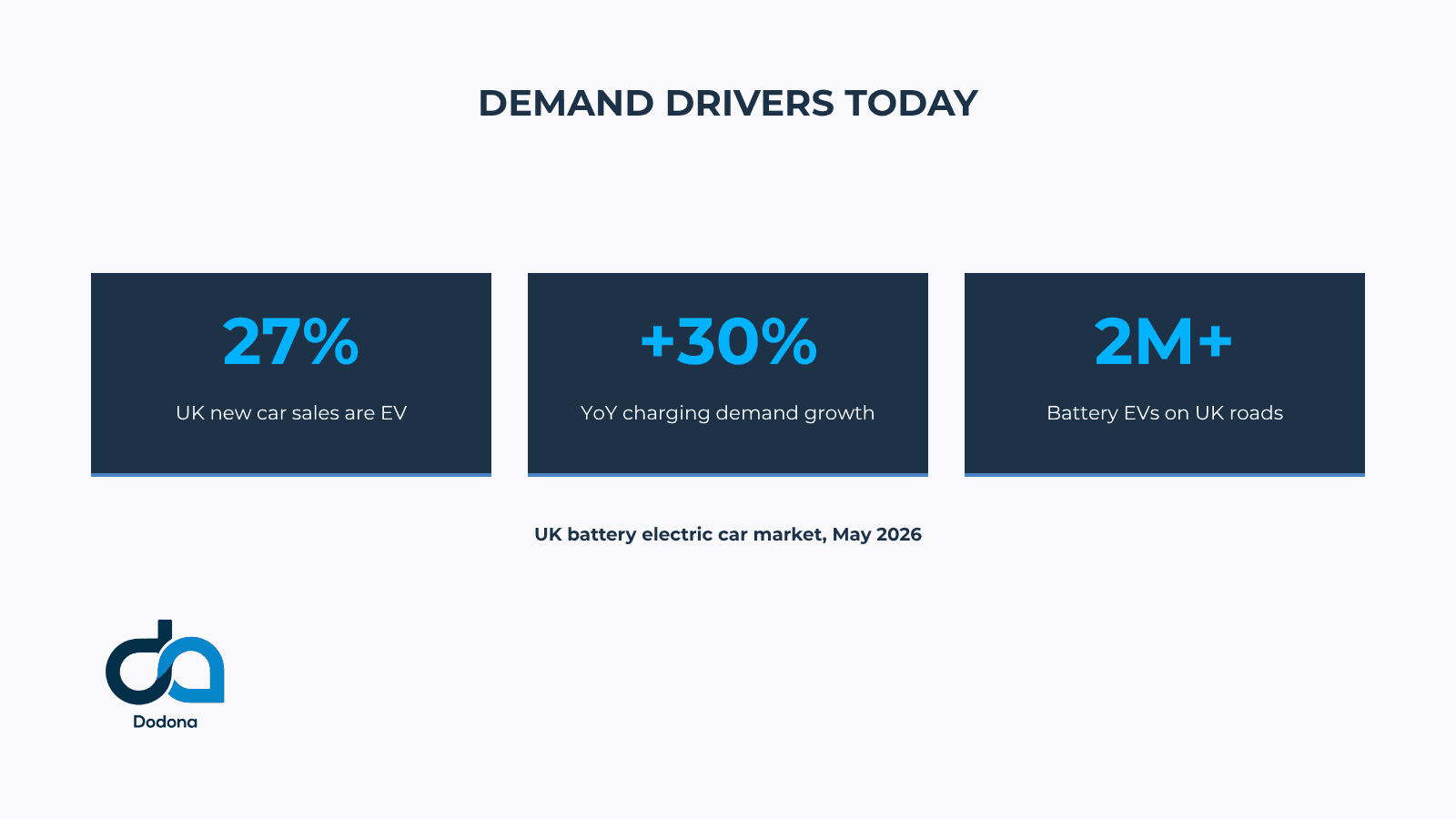

And then this spring, demand started to increase. Battery electric cars took around 27% of the UK new car market in May, up more than 30% on the year before, and March set a record. More than two million fully electric cars now drive the UK roads. The reasons are worth reading closely. Part of it is cheaper, more practical models, with mainstream brands leading rather than premium badges. The rest is fuel prices. Conflict in the Middle East has pushed petrol and diesel up, and a driver already weighing an electric next car now has one more reason to switch. That is a different buyer from the early adopter, and there are far more of them.

This is where operators get caught out. A surge in demand lifts the good sites and exposes the bad ones. It does nothing for a charger in the wrong place, and it does not repair a cost base that never made sense. More cars plugging in will not save a network someone built solely to hit a deployment target and overpaid for the site.

Why a charging network makes poor collateral

Which brings me to the money. Specifically, loan vs equity financing. A loan needs collateral, and a charging network makes poor collateral. Think about where the spend goes when you build a site. Only one part buys the hardware. The rest disappears into trenching, the grid connection, the civil works, the months of groundwork nobody ever sees. If the business fails, a lender can take the chargers. They cannot dig the cable back out of the ground, re-expose the concrete, or recoup the cost of the grid upgrade. That value stays with the landowner. Add a track record that gives a lender little basis for modelling when the loan gets repaid, and the debt comes off the table. That leaves equity, and today's equity investors ask a sharper question. Not how fast can you build, but when does the network start making money?

During the boom, almost nobody had to answer that. The deal was blunt. Here is the cash, put 300 chargers live by year-end. Quantity over quality. I sat in plenty of conversations where the whole target was a deployment number, and the honest reply, yes, but not at any price, rarely won the room. Operators bought sites in 2023 and 2024 at prices that only worked on demand that had yet to arrive. In hindsight, that was a bad trade. The operators who held their discipline and missed the deployment numbers back then look like the sensible ones now.

The industry has run this cycle before

We have watched this film before. When the railways and telecoms networks were first built, many early operators overspent, got overleveraged, and were later forced to sell their assets for pennies on the dollar. The businesses that did well were often the ones that bought those assets cheaply, out of the wreckage, and ran them with discipline. Charging is tracking the same path. Expect more networks to come to market this year, and the numbers are getting harder to hide.

So the operators who attract money now are the ones who already run as though money is scarce. The pattern repeats every time I look at a healthy network. They run more sites per person. They have not built a department for every problem, and they can tell you the economics of every site they operate. That discipline shows up twice. In how well they run what they have, and in how carefully they choose where the next charger goes. Those operators are still growing. They are still raising. That is not luck.

Fleets are the second engine, and most operators miss it

There is a second engine here, and it is the one most operators underplay. Fleets.

Electric vehicles are getting bigger and cheaper. Vans, heavier commercial vehicles, the workhorses cities run on, all of it is now within reach for buyers who order in volume. A large number of fleets are working through electrification right now. Three forces push them: net-zero commitments they set for themselves, city rules that make older diesels steadily more expensive to run, and major clients mandating net-zero from certain dates onwards.

Electrifying a fleet only works when three groups start working together, and most of them are used to ignoring each other. Vehicle makers and dealers are the first. Selling the van is no longer the whole job, because the fleet manager's next question is how to charge it. The maker or dealer who can answer that, or partner with someone who can, takes a share from those who hand over the keys and walk off. There is a real opening for dealers here right now. Fleet operators are the second. A fleet cannot simply order new vehicles and hope. They need a partner to help them work out which vehicles to switch, in what order, and how they will charge, grounded in how the fleet runs in practice rather than in a brochure. Charging providers are the third. The group spans public network operators and firms that build and run private depots. For an operator, a fleet is a heavy, predictable user. A deal with one guarantees energy offtake and lifts utilisation on sites that would otherwise sit idle between peaks.

Same vehicle count, completely different infrastructure

There is a catch, and it is the whole game. You cannot serve a fleet with a generic product. Say a depot has 24 vehicles to charge. If they trickle back one at a time through the evening and they need to be full by morning, you build one kind of site. If they all return at noon for a fast recharge and have to be ready again in 1 hour, you build something else entirely, with far more power and a much tighter energy plan. Same vehicle count, completely different infrastructure and economics. Read it wrong, and the fleet ends up unhappy as they have built the wrong thing.

The strategic point follows from that. Fleet vehicles cover far more miles than the average private car, so they pull a share of charging energy well above their share of vehicles on the road. An operator with no fleet-ready offer has quietly written off that demand. It is a decision, even when nobody set out to make it.

The work that Dodona was built to do

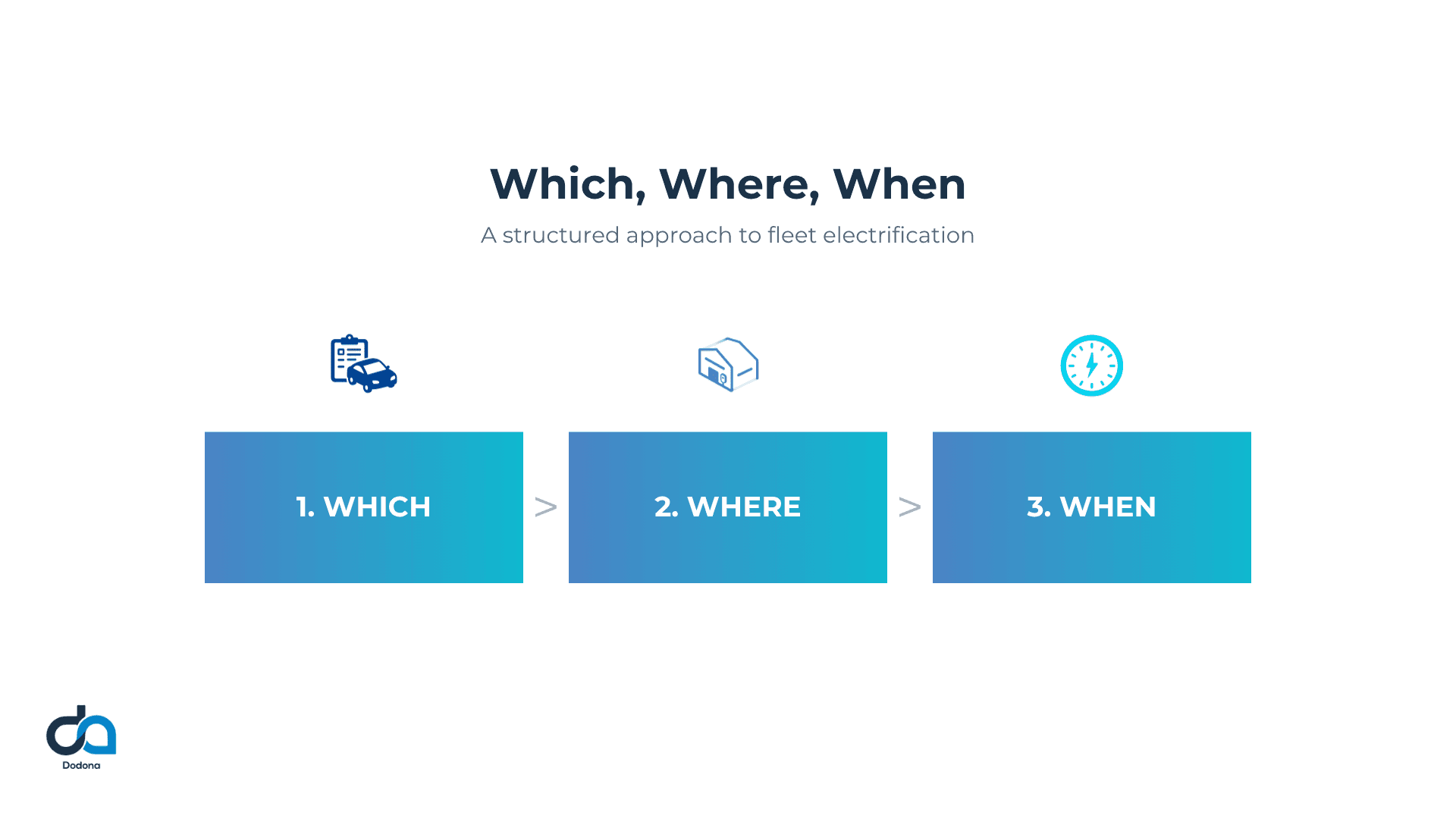

Connecting those three sides is the work done at Dodona, and we ground every decision in real demand rather than guesswork. For fleets, our Which, Where, When framework takes the questions in the order they arrive: which vehicles to transition first, where they will charge, and when to move.

The deploy-fast decade is over. The next one rewards whoever runs the tightest network and reads demand most clearly. The operators who also treat fleets as real customers, not an afterthought, will pull ahead. The money has already worked this out. The ones who make it through will be the operators who do the same before their next raise, not after.

One question is worth sitting with before that raise. Can you point at your network and say which sites make money and which lose it? And do you know where the next charger has to go to earn its place? That is the work we do at Dodona. If it is the question in front of you, let's talk.

Read More

Which. Where. When. A Framework for Fleet Electrification

Most fleet operators know electrification is coming. The harder problem is figuring out where to start and how to structure something that still makes sense three years from now, when the market looks different.

That tension comes down to three questions. Which vehicles can make the switch? Where will they charge? When to move and in what order? These questions look simple in isolation. In practice, they are intertwined in ways that make it almost impossible to answer one without the other.

The answer to which vehicles to electrify first depends on where your charging infrastructure will be located. Your infrastructure decisions depend on how your vehicles move. Your phasing depends on both. Get one wrong, and your vehicles will not operate.

Which vehicles can transition

Not every vehicle in your fleet is ready at the same time, and trying to transition them all at once is a reliable way to run into trouble.

The vehicles that switch cleanly are those running shorter, more predictable routes. Vehicles that return to a depot or home location overnight. Drivers who dwell somewhere long enough to top up. Routes where daily mileage sits comfortably within the range of available EVs.

Identifying those vehicles requires actual data. Telematics records that show how far each vehicle travels, where it stops, and for how long. Upload that data, and you can see, vehicle by vehicle, which ones would have had range issues over the last year if they had been running on electric. The ones with no issues are your starting point.

The ones that do not make the cut yet are not failures. They just need a different approach and likely a different timeline. Some will become viable as public networks grow around the routes they use, or as you build your own charging infrastructure. Others will get easier as EV ranges keep improving: the average in 2020 sat at around 330 to 420 kilometres; by 2025, it had moved to 380 to 500 kilometres. What looks difficult today often looks straightforward two years later.

This is not about being conservative. It is about having confidence that you will have an operational electric fleet.

Where will they charge

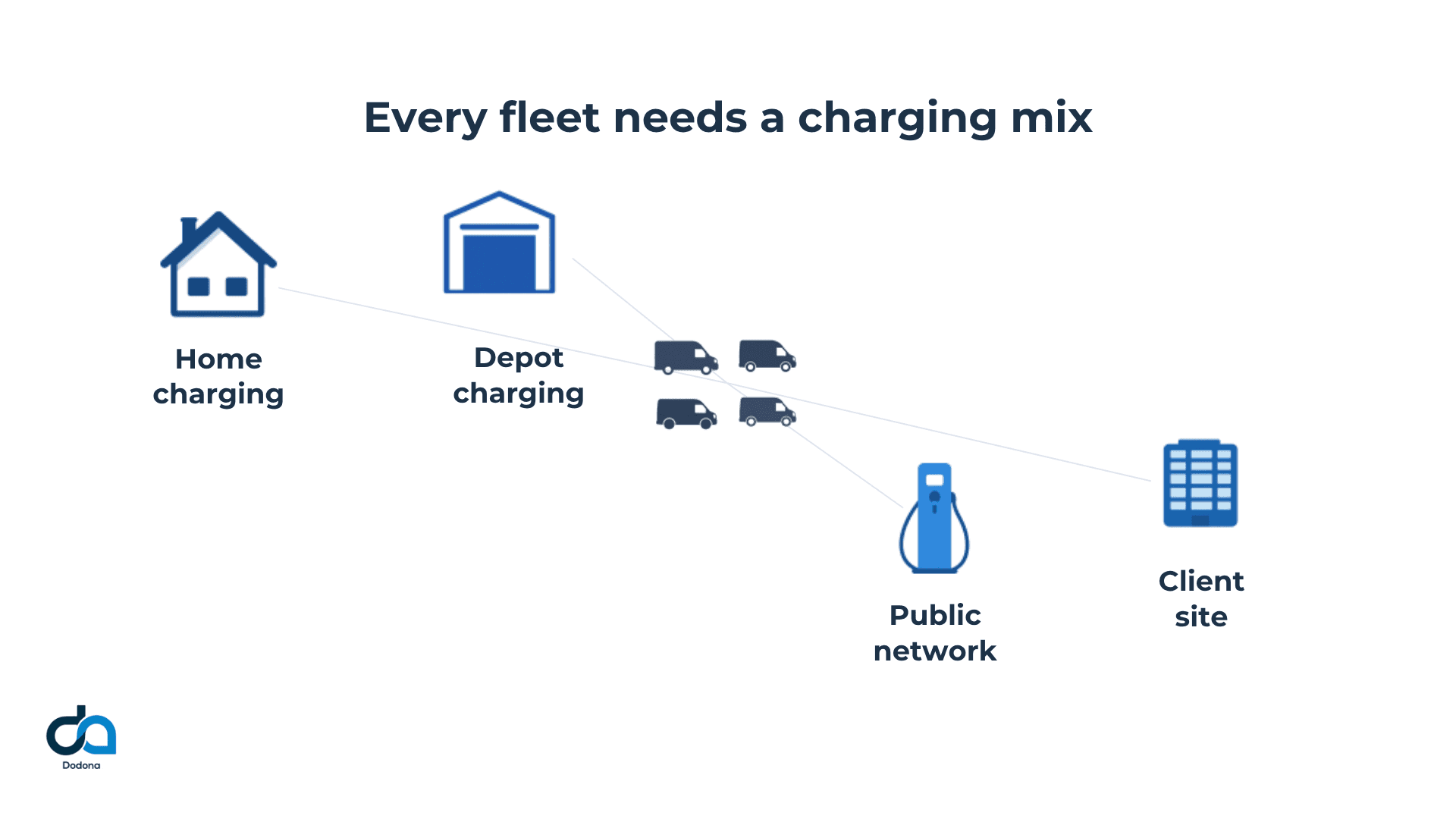

An electric vehicle can only operate if it can charge. This is where most electrification plans run into their first real problem.

For any fleet, multiple charging options operate in parallel: at home, at depots or offices, at client and partner locations, and on public or dedicated networks. Each plays a different role, and the right mix depends entirely on how your fleet operates.

Home charging is the simplest lever for the right vehicles. A driver plugs in overnight and leaves with a full battery every morning. For vehicles with moderate daily mileage and drivers who have a home charging station, that is often all you need. The infrastructure cost is relatively low, and the logistics are straightforward. But not all drivers have driveways and the option to charge at home.

Depot charging handles vehicles that need more. A warehouse, a logistics hub, an office car park: if vehicles dwell there for a meaningful window, chargers there make use of time that would otherwise be wasted. But depots can be constrained by power availability, so you may not have enough capacity to charge all vehicles at once.

Public networks can sometimes fill the gaps. A vehicle that runs long distances needs a reliable on-route recharging option. The question is which public networks actually cover the routes your fleet uses, and whether partnering with one over another gives your vehicles better access or better commercial terms.

There are also questions worth thinking through before you commit to anything. Do you need to build your own charging infrastructure beyond your locations? Can you charge at your clients or partners locations? What does it mean for your business if a vehicle cannot be recharged at the time planned?

The answer is almost always a mix. If you want to go deeper on how different charging scenarios stack up against each other, the tradeoffs between depot, home, public, shared, and semi-public charging are covered in detail in the Which charging scenario suits my fleet article we posted previously.

When to make the switch

Timing matters. Starting with the wrong vehicles undermines confidence in the programme as a whole. Starting without considering the charging infrastructure creates the same problem from a different angle.

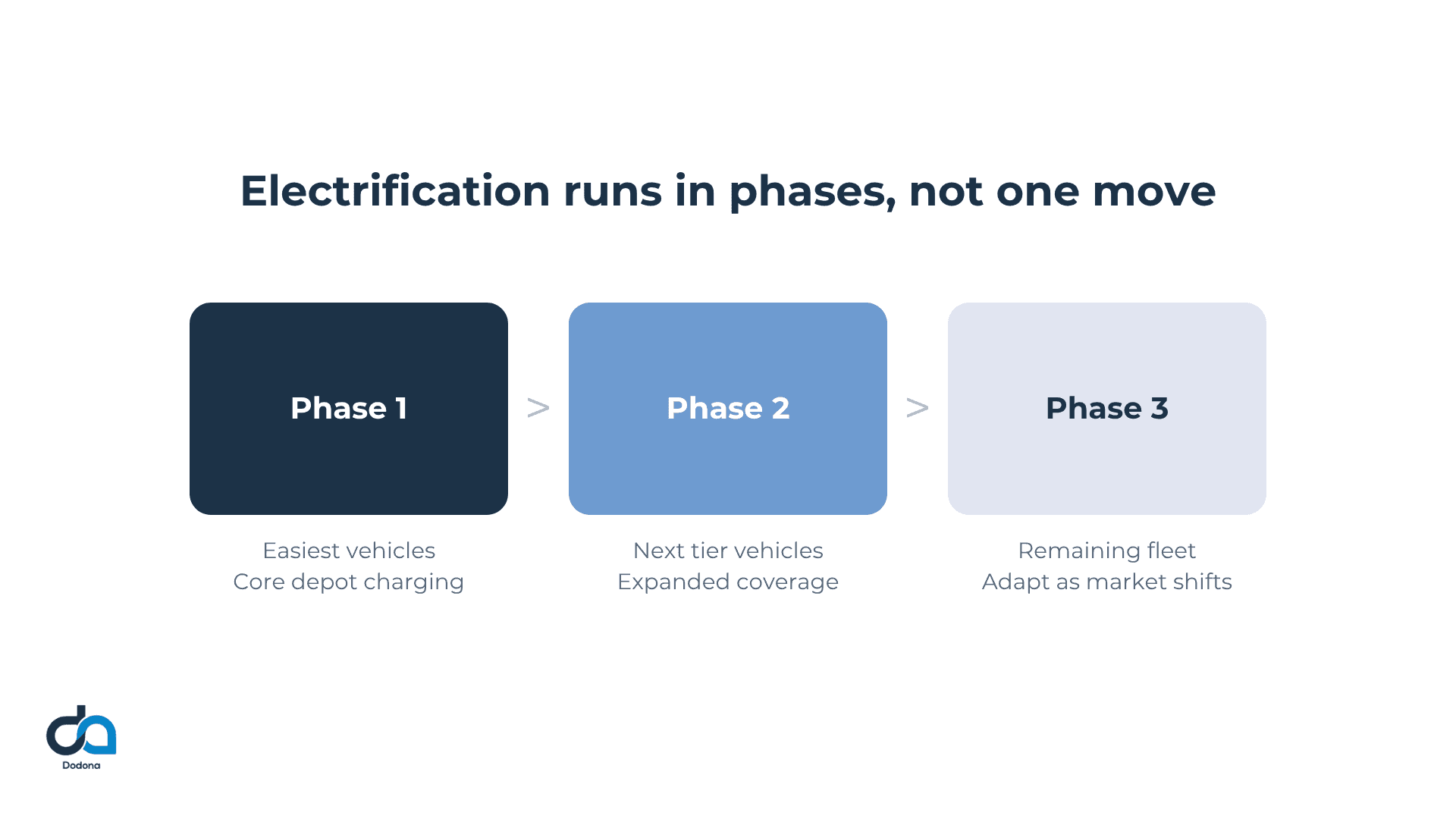

Fleet electrification is not a two-week Excel exercise. For most fleets, replacing the entire fleet takes seven to ten years. Vehicles have amortisation cycles of seven or eight years, which means each year roughly a seventh of the fleet becomes a candidate for replacement. You are not making one big decision. You are making a sequence of smaller ones across a longer time horizon.

Phase one should be tight and well-studied. You know which vehicles you are electrifying, which charging infrastructure you are installing, the costs, and the rollout. Start with what is genuinely ready and do it properly.

Phase two is typically more directional. You have a solid working plan, but you hold it loosely, because by the time you execute it, the market will have moved. EV ranges have been shifting steadily. Charger costs have come down. Public networks have grown. The cases that were not ready in phase one will look different by then.

Phase three and beyond should leave room to adapt. A plan that cannot flex to a rapidly changing market is not a plan. It is a liability.

The goal is not a detailed ten-year fixed roadmap. It is a structured phased plan with enough flexibility in the outer years to respond to a market that will undoubtedly look different by the time you get there.

Why do most tools only answer one of the three

There are tools that help you optimise routes for individual vehicles. There are tools that help you decide where to put chargers at a single site. What has been missing is something that looks at which, where, and when together and maps them onto how your fleet actually operates.

Fleet management software was built around different problems. It understands scheduling, driver management, and maintenance cycles. It was not built for the new layer of complexity that electrification adds: understanding which vehicles are ready, mapping them against actual charging coverage, and sequencing the entire electrification project across multiple sites and years.

Dodona comes from a long-standing heritage. The platform was built to help charging point operators understand where and how to deploy EV charging infrastructure. That same analytical foundation, built on real charging data, real network coverage, and real vehicle behaviour, is what fleet operators need when they are working out what an electrification project actually looks like for their own operation.

The CPO fit analysis overlays your fleet's actual stop locations and estimated battery states onto the public charging infrastructure in your area. You can see exactly how well different networks cover your routes and where depot or home charging needs to fill the gaps. That connection between vehicle behaviour and charging reality is what turns a transition plan into something you can actually execute.

What this looks like in practice

A fleet of 180 vehicles. You upload the telematics data, the records of where each vehicle went and when. The platform analyses it and shows you, for each vehicle, how that driving pattern would have worked with a specific EV model. Most of them are green. A handful have days where they would have needed a top-up somewhere. One or two have routes that are genuinely difficult.

You can immediately see which vehicles to electrify first. You can see which public charging operators have sites along the routes your difficult vehicles take. You can add a depot location and watch the analysis update. Fewer range concerns. A clearer picture of what infrastructure you actually need.

Then you structure it into phases. Phase one: the easy vehicles, depot chargers at your main site, and home charging for drivers who can use it. Phase two: the next tier, expanded public network coverage, potentially a second site. And so on.

That is the conversation Dodona makes possible. Which vehicles. Where they charge. When to move. Answered together rather than one at a time in a vacuum.

Book a 30-minute demo and bring your questions. No commitment required:

Read more about fleet electrification on the Dodona blog.

Explore our new fleet lading page and read the case study.

Dodona helps fleet operators make better EV charging decisions. Clients include E.ON Drive, Mercedes-Benz, Bosch, and TotalEnergies.

Read More

One Size Does Not Charge All: Which charging scenario suits my fleet?

Fleet electrification is not simply a matter of replacing one vehicle with a comparable model. Electric vehicles represent a fundamental shift in how fleets operate, not just in what they drive, but in how, where, and when they refuel. With a combustion vehicle, the question of energy was largely invisible: fill up at the nearest station and get back on the road. With EVs, that question becomes central to every operational decision.

Fleet electrification has reached an inflection point where the question is no longer whether to transition to electric vehicles, but how to charge them effectively. And that question, where will we charge? It is far more complex than it first appears. There is no universal answer. The right charging scenario depends on operational patterns, duty cycles, site constraints, and grid capacity, and each option comes with its own distinct trade-offs.

The problem

Fleet managers consistently report confusion about where to begin their electrification journey. The challenge stems from a fundamental mismatch: what works brilliantly for office-based vehicles fails catastrophically for high-utilization delivery fleets or emergency services operating around the clock. A post office fleet that returns vehicles each evening faces entirely different constraints than sales representatives whose company cars never visit headquarters.

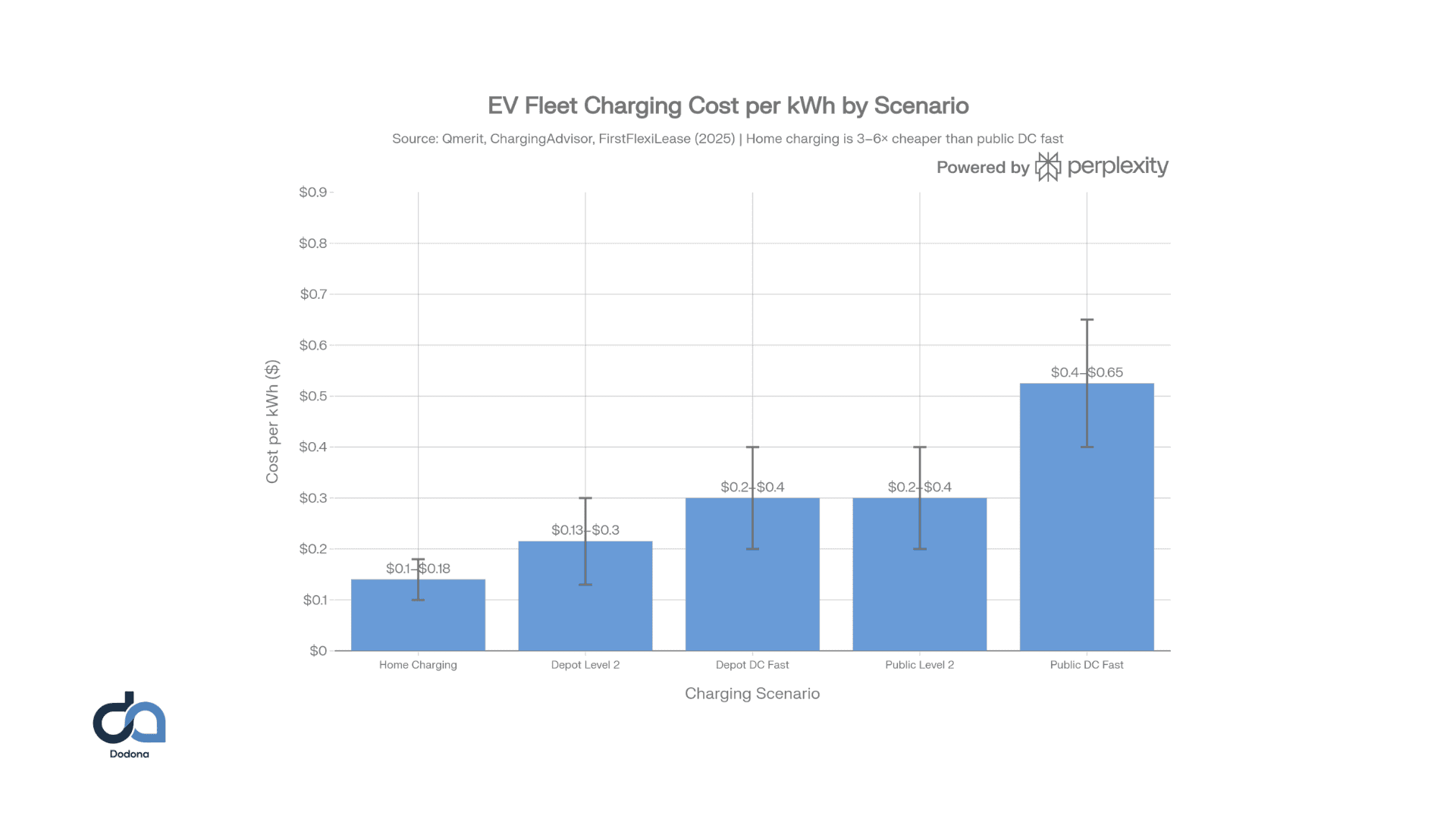

The stakes are considerable. Recent data from UK fleets show that charging strategy directly impacts operational costs: public charging sessions accounted for only 27% of total charging events but consumed 57% of fleet charging budgets, with costs averaging 81 pence per kWh compared to 25 pence for home charging. A poor charging strategy can transform an otherwise cost-effective EV deployment into an economic liability.

Understanding the charging spectrum

Depot and office charging

Depot charging represents the most straightforward option for fleets with predictable operational patterns. Vehicles park at a central location during operational hours (aka people in the office) and during non-operational hours (typically overnight), where AC chargers (7-22 kW) replenish batteries over 8-12 hours.

This approach works exceptionally well for office-based fleets, municipal vehicles, and any operation where vehicles consistently return to a base location. Installation costs range from $3,500 to $15,000 per charging port for AC equipment, with networked systems adding $500-$1,500 per port for remote monitoring and load management capabilities. Despite higher upfront investment, depot charging delivers the lowest per-kilowatt-hour costs and eliminates the markup premiums charged by public networks.

Home charging for return to home fleets

Home charging addresses the distributed fleet challenge by leveraging employees’ residential locations as charging infrastructure. Drivers charge company vehicles overnight at residential electricity rates, which are typically the most economical option. UK fleet data from 2025 shows home charging averages 25 pence per kWh, compared with 81 pence for public charging, more than three times cheaper.

This model requires establishing reimbursement systems to compensate employees for electricity consumption, with sophisticated tracking platforms now enabling accurate session‑level billing. In certain jurisdictions, such as California, home charging reimbursement is subject to labor code requirements.

The strategic advantage extends beyond cost savings. Home charging eliminates range anxiety for daily operations, ensures vehicles start each day fully charged, and distributes grid load across residential networks rather than concentrating demand at depots. Rightcharge data indicates that shifting a single vehicle from public to home charging can save up to £1,300 annually.

However, this approach relies on one key condition: employees must have a dedicated off‑street parking space, such as a private driveway or garage, where they can safely install and use a home charger. In areas with limited off‑street parking or where employees rely on on‑street or public parking, home charging is not feasible for those drivers, and fleets must fall back on depot, shared, or public charging alternatives.

Public charging networks

Public charging offers maximum flexibility with minimal infrastructure investment; fleets simply pay per session at third-party-operated charging stations. No capital expenditure, site preparation, or electrical upgrades required.

Despite these advantages, public charging carries substantial economic penalties. Analysis shows public DC fast charging costs 30-48 cents per kWh compared to under 13 cents for depot charging. The 2026 State of Fleet Charging report clearly documents this: public sessions accounted for 27% of charging events but 57% of total spend. Beyond cost, reliability concerns persist; some surveys report 25% of public chargers are non-functional at any given time.

Public infrastructure serves strategic roles as backup capacity, supplemental range extension for exceptional trips, and temporary solutions during early fleet transition phases. However, building fleet operations around public charging as the primary strategy guarantees significantly higher operating costs.

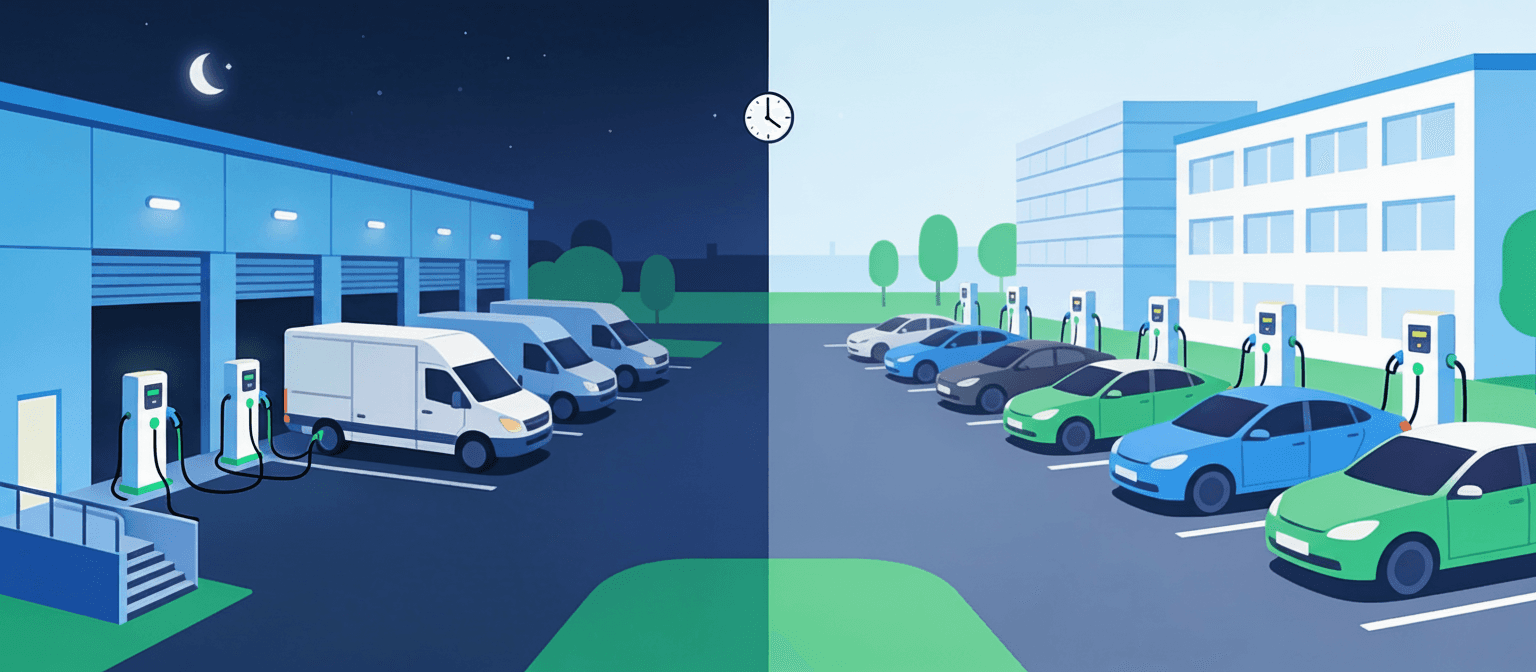

Shared depot charging

Shared depot arrangements enable multiple fleet operators to utilize common charging infrastructure, particularly effective when operational schedules create complementary usage patterns. A logistics company operating delivery vehicles from 6 AM to 10 PM can share facilities with an office fleet charging from 8 AM to 6 PM, maximizing infrastructure utilization without scheduling conflicts.

The UK's shared depot network provides concrete evidence for this model, with 31 member organizations, including municipal councils, emergency services, and private operators. The network recorded more than 200 cross-depot charging sessions per month, demonstrating both technical feasibility and operational acceptance.

Shared infrastructure reduces per-vehicle capital costs through pooled investment, accelerates deployment timelines by leveraging existing sites, and increases network resilience by providing geographic charging redundancy. However, implementation requires careful coordination of access management, energy billing allocation, and maintenance responsibility sharing.

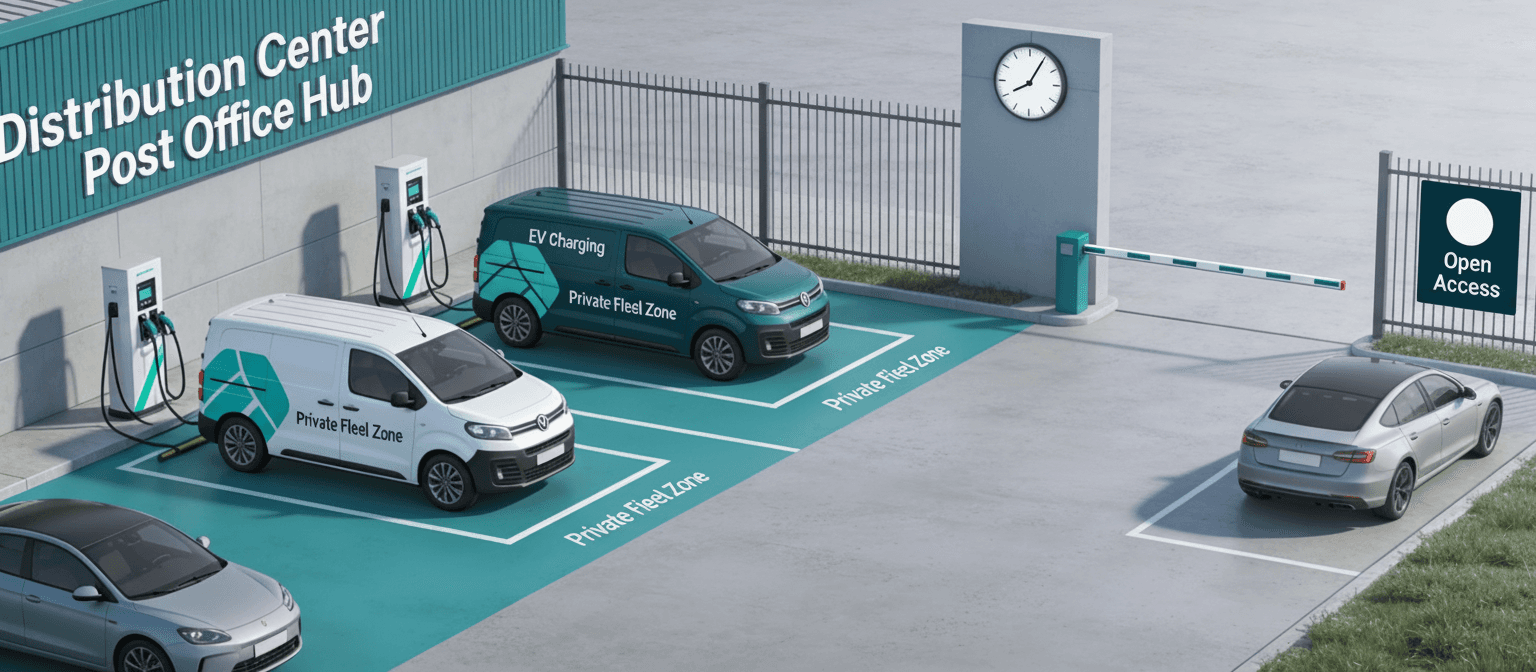

Semi-public charging hubs

Semi-public models position fleet charging infrastructure to generate dual revenue streams, serving captive fleet operations during primary hours and opening to the public during off-peak periods. A postal service might operate vehicles from 7 AM to 8 PM using depot chargers, then monetize that same infrastructure for public access from 8 PM to 7 AM.

Daimler's TruckCharge network exemplifies this approach at a commercial scale. Logistics companies like Wessels Logistik deploy charging infrastructure sized for fleet requirements, then sell excess capacity to other commercial users and the general public during downtime. Shell's integrated truck charging network similarly blends private fleet operations with public access, creating what they term built by fleets, for fleets infrastructure.

This model works best for operations with clear temporal boundaries, retail locations, distribution centers with defined shift patterns, or service facilities with predictable closures. The additional revenue can significantly improve infrastructure ROI, but it also introduces operational complexity in access control, billing systems, and mixed‑use management. The challenge with this model is that it requires someone to operate and oversee the charging hub, including managing access, resolving issues, and coordinating between fleet and public users.

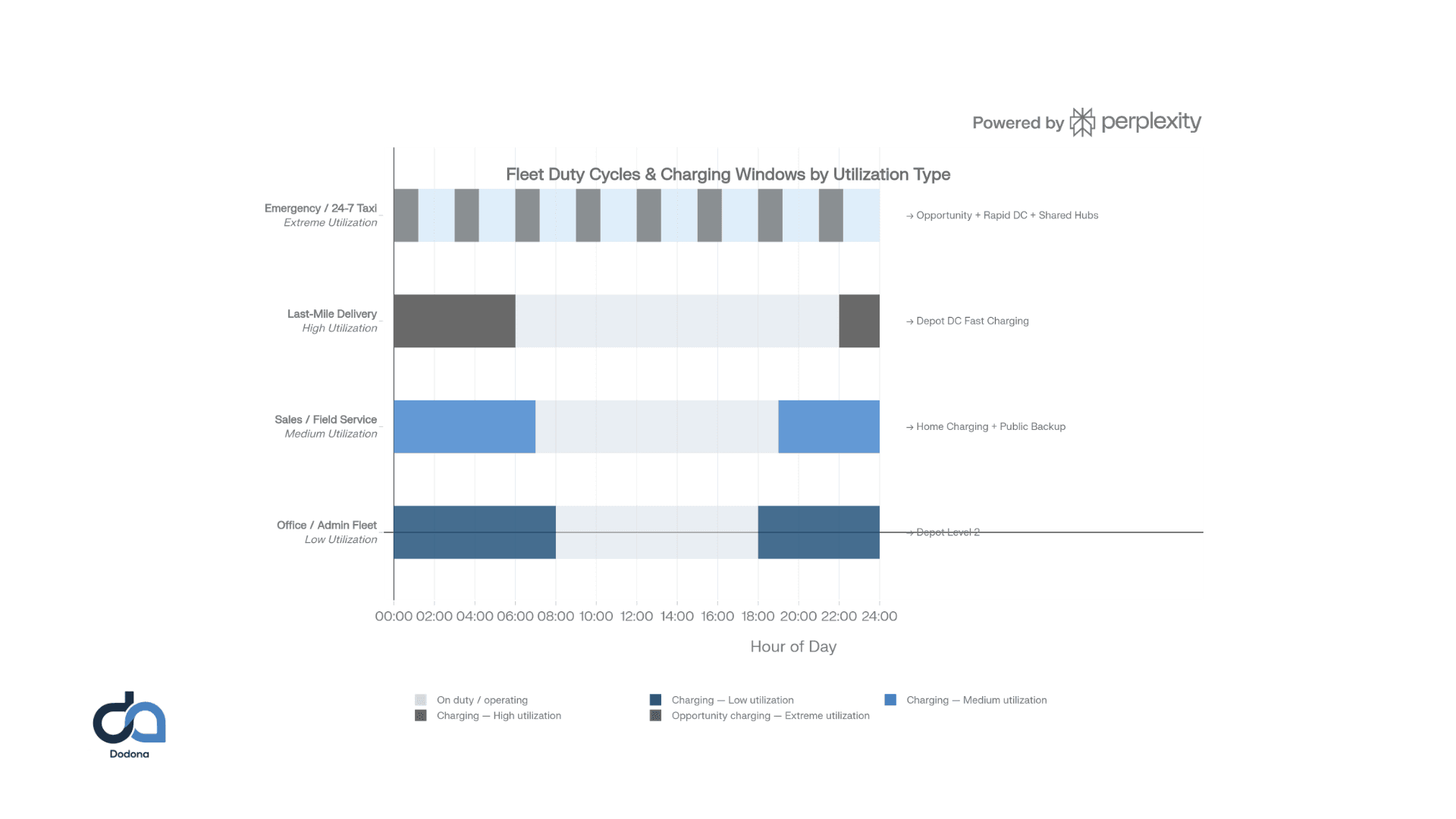

The duty cycle imperative

An optimal charging strategy depends fundamentally on vehicle duty cycles, the operational patterns that define when vehicles operate and when they're available for charging. Misalignment between duty cycles and charging strategy results in either underutilized, expensive infrastructure or insufficient charging capacity, constraining operations.

Low-utilization fleets with vehicles parked at depots for 8-12 hours are well-suited to AC charging. Administrative fleets, municipal inspection vehicles, and office-based pool cars fall into this category. Charger-to-vehicle ratios of 1:2, 1:3, or even 1:4 are the norm, and suffice when paired with smart load management, as overnight dwell times provide ample charging windows.

Medium-utilization operations involving distributed territories and moderate daily mileage; sales fleets, field service, regional delivery; optimize around home charging, supplemented by public fast charging for exceptional circumstances. These vehicles rarely visit depot locations during operational hours, making centralized infrastructure impractical.

High utilization fleets operating intensive daily schedules with predictable depot returns require depot-based DC fast charging combined with sophisticated load management. Last-mile delivery, local trucking, and municipal transit fall under this category. Managed charging systems reduce peak electrical demand by 25% and cut operational costs by 37% compared to unmanaged approaches.

Extreme use cases, emergency services, 24/7 taxi operations, and continuous delivery networks pose the most challenging requirements. These fleets swap vehicles rather than drivers, meaning assets remain in continuous service. Solutions require a combination of opportunity charging, rapid DC infrastructure, and, potentially, multi-fleet shared hubs to maintain 24/7 charging availability.

Grid capacity: The invisible constraint

Even perfectly designed charging strategies collide with physical reality at the utility connection point. Distribution grid capacity is often the primary constraint on fleet electrification, particularly for large-scale deployments.

A medium-duty delivery fleet transitioning 50 vehicles might require 2-5 megawatts of new electrical capacity. If that capacity doesn't exist at the depot, requesting utility upgrades can trigger multi-year processes. The UK's connection queue stood at 732 gigawatts as of September 2024, with some projects facing 5+-year timelines.

Industrial zones typically offer better grid access than commercial or residential areas, making relocation more practical than waiting for utility upgrades. Alternatively, phased transitions deploying 20-30% of the target fleet size can operate within existing capacity while upgraded connections proceed in parallel. This approach requires early coordination with utility operators; fleet managers should engage distribution network operators 12-24 months before vehicle deliveries.

When grid constraints prove insurmountable, alternative solutions include battery energy storage systems that buffer peak demand, off-grid mobile charging solutions deployable in weeks rather than years, or shared charging hubs at grid-ready locations, even if geographically suboptimal.

Economics: The charging cost hierarchy

Charging location fundamentally determines operational economics. The cost hierarchy from most to least economical follows a clear pattern:

Home charging offers the lowest per-kWh cost at residential electricity rates, typically 25 pence per kWh in the UK and under 13 cents in the US. Zero infrastructure capital requirements for fleet operators, though employee reimbursement programs require administrative overhead.

Depot AC charging costs slightly more per session due to commercial electricity rates, but eliminates public charging markups while maintaining complete operational control. Total installed costs range from $3,500 to $15,000 per port, depending on site conditions and networking requirements. Off-peak charging windows can deliver 30-50% savings compared with peak-hour electricity rates.

Depot DC fast charging increases both capital costs ($55,000-$120,000 per station) and per-kWh expenses due to demand charges on peak power draw. However, fast charging enables operations that require rapid turnaround times, which Level 2 charging cannot support.

Public DC fast charging sits at the top of the cost hierarchy, with session prices ranging from 30 to 81 pence per kWh, depending on provider and location. The convenience of zero infrastructure investment comes at a 3-6x premium over home or depot charging.

Fleet analysis from 2025 shows that optimal strategies typically blend 2-3 charging types, perhaps 70% depot charging, 20% home charging, and 10% public as backup. This mixed approach balances capital efficiency, operational flexibility, and per-session economics.

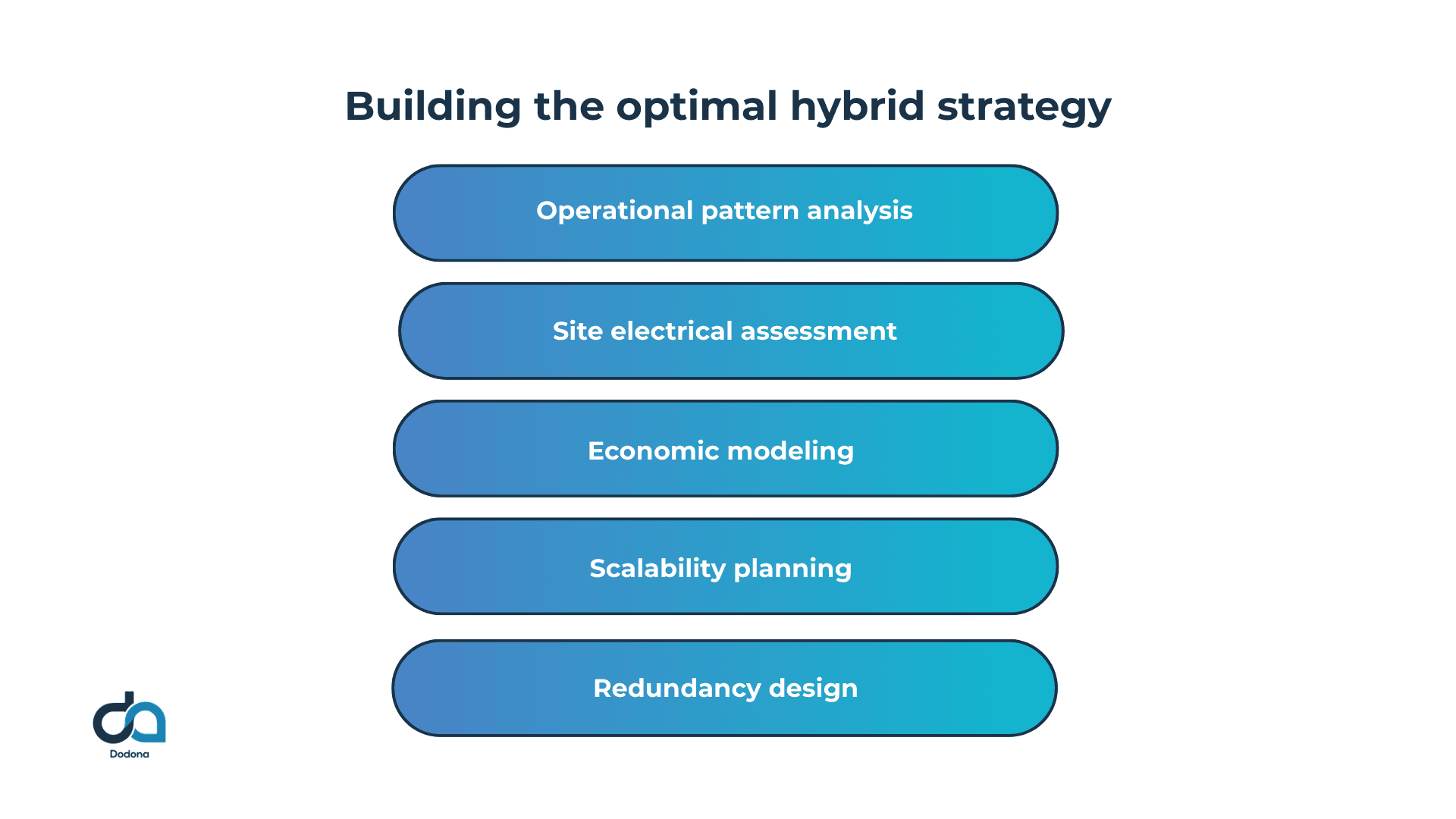

Building the optimal hybrid strategy

No single charging scenario fits all fleet types, which explains why successful deployments typically combine multiple approaches. The optimal strategy emerges from a systematic analysis of several interconnected factors.

Operational pattern analysis begins with detailed duty-cycle mapping, covering when vehicles operate, where they park, how long they remain stationary, and whether patterns vary by day of the week or season. This reveals charging windows and identifies whether depot, home, or distributed charging aligns with vehicle availability.

Site electrical assessment determines available capacity, upgrade costs, and utility coordination timelines. This analysis often shows that grid constraints, rather than vehicle or charger limitations, drive deployment pace.

Economic modeling compares the total cost of ownership across charging scenarios, accounting for infrastructure capital costs, installation expenses, electricity rates, demand charges, and the value of operational flexibility. The lowest per-kWh cost doesn't always yield the lowest TCO when infrastructure investment and utilization rates are factored in.

Scalability planning ensures initial deployments can expand as fleet electrification progresses. Electrical service sizing, physical space allocation, and network architecture should accommodate future growth without requiring complete rebuilds.

Redundancy design recognizes that failures in charging infrastructure directly impact fleet operations. Charger-to-vehicle ratios of 1:2, 1:3, 1:4 provide buffer capacity, while access to backup charging options (public networks, shared facilities) maintains operations during primary system outages.

The most successful strategies combine depot charging to meet the bulk of fleet requirements with home charging for distributed vehicles and public charging as operational backups. Smart load management systems optimize charging schedules to minimize demand charges while ensuring vehicles are ready for service when needed. This layered approach balances capital efficiency, operational reliability, and cost optimization across the entire fleet lifecycle.

How Dodona can help you find the right solution for your fleet

There is no single right answer for every fleet. The best charging scenario depends on your routes, duty cycles, sites, and grid constraints. Getting it wrong can lock you into years of higher costs and operational friction.

That's the problem we focus on. We don't sell a predefined setup. We help you understand your data and build a charging strategy around what it actually shows.

What we do

Map your duty cycles

Using your real operational data, mileage, routes, and dwell times, we model when and where your vehicles can realistically charge. That determines whether depot, home, shared, or public charging makes sense, and in what combination.

Run scenario comparisons

We test options against each other: depot-only, home with public backup, shared hub, semi-public. You see the impact on costs, uptime, and grid demand before you commit to anything.

Right-size your infrastructure

Too many chargers are a waste of capital. Too few creates bottlenecks. We help you start at 20-30% of your target fleet size within your current grid capacity, and plan expansion as connections come online.

How it looks in practice

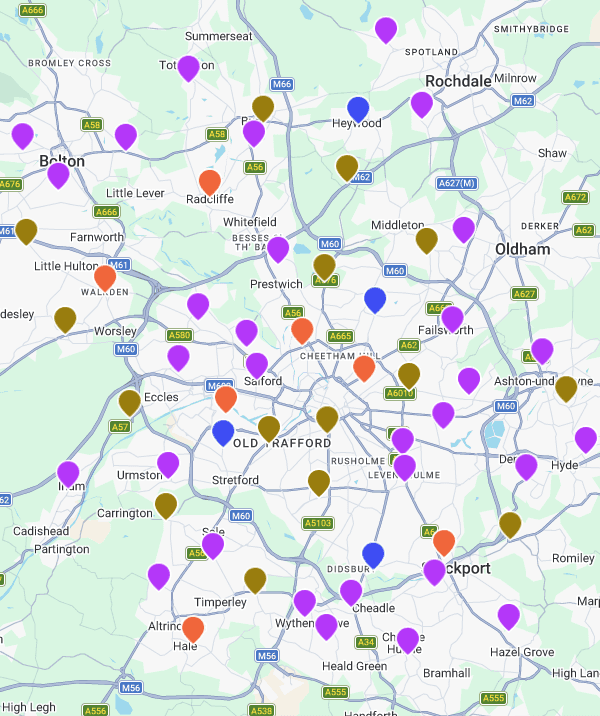

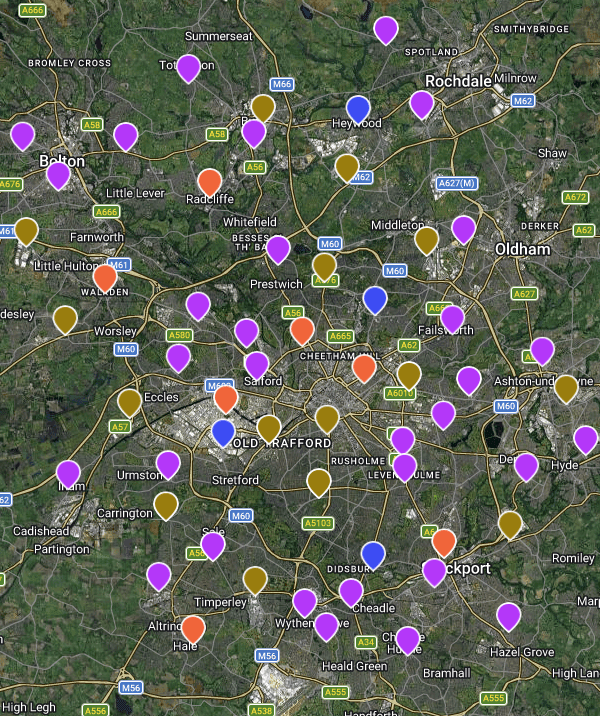

Every fleet looks different on a map. Before recommending anything, we plot your telematics data geographically so the patterns become visible rather than assumed.

Every pin is a vehicle. Colour shows where and how it charges across the operating area.

The zoomed-out view tells you where your fleet actually lives. You can see immediately whether vehicles cluster near a depot, spread across a wide territory, or sit in locations where home charging is the realistic option.

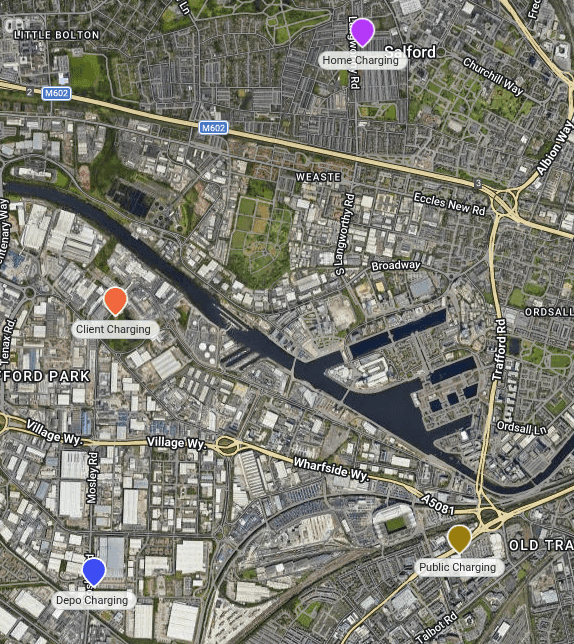

Zoom in on any vehicle, and the picture gets more specific.

One vehicle, three charging touchpoints: home, depot, and client site. Public charging fills the gaps.

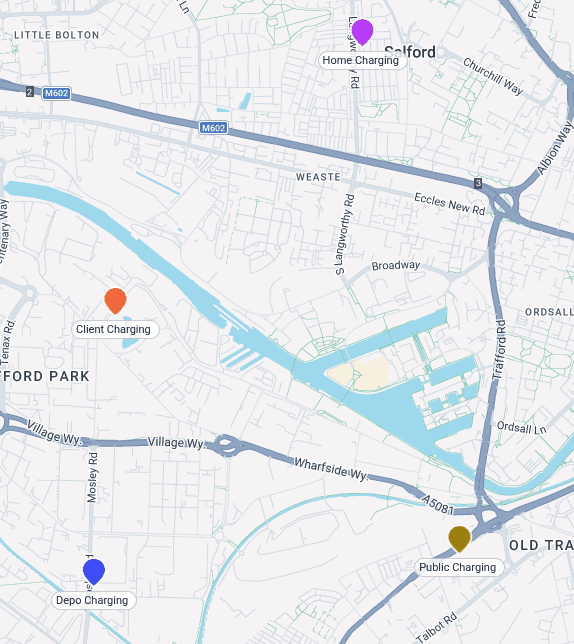

A single driver in this fleet charges at four distinct locations. That mix has direct cost and reimbursement implications, and tells you exactly what infrastructure actually needs to be built.

The trip data adds the time dimension.

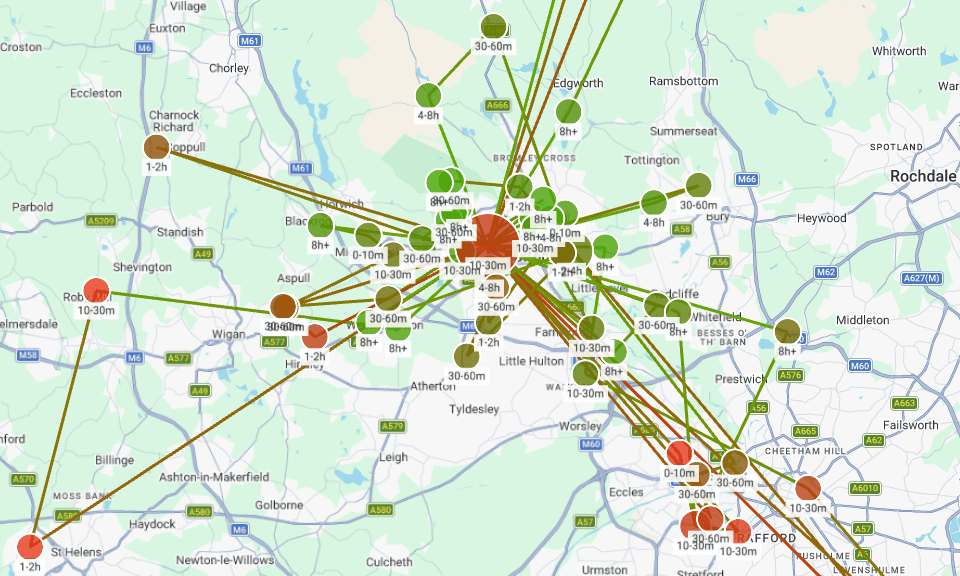

One vehicle's trips, with dwell time at each stop. Green means long enough to charge. Red means not.

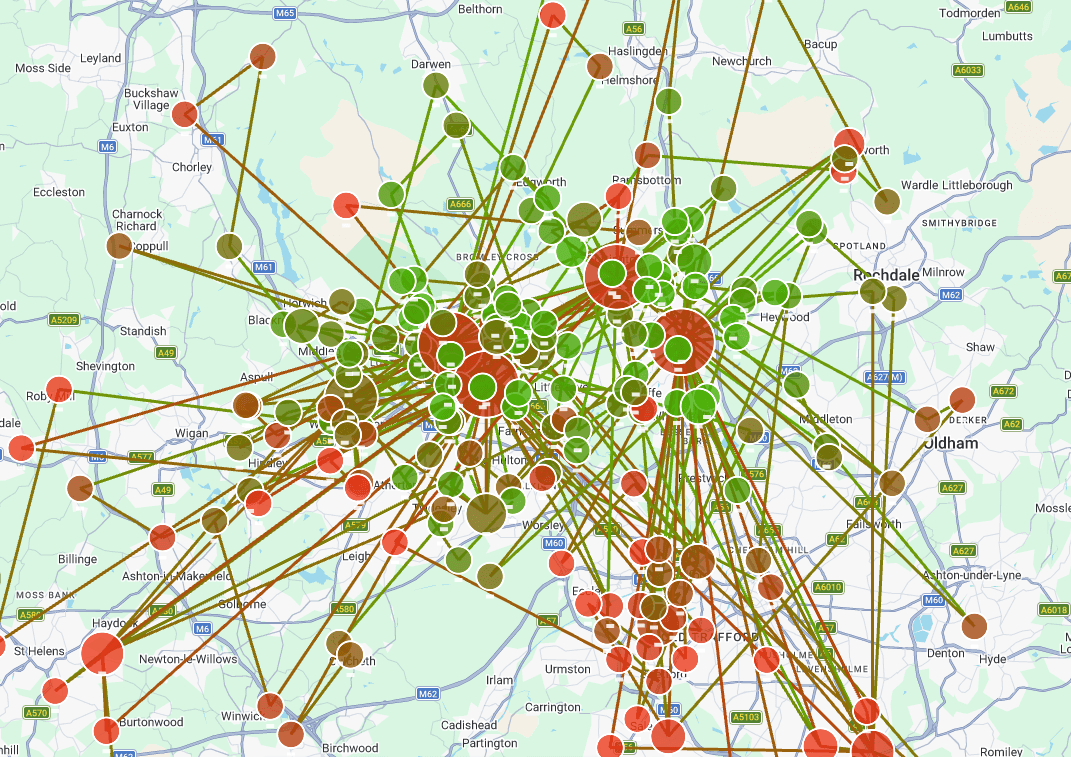

The same view across the entire fleet. Where the red concentrates is where your charging gaps are.

Dwell time is the variable most fleet managers overlook. A vehicle parked at a client site for four to eight hours is a charging opportunity. One stop for ten minutes is not. Seeing this across every vehicle and every stop tells you far more than a spreadsheet of daily mileage figures.

Ready to find your mix?

If you're weighing up a depot investment, considering home charging for your distributed drivers, or trying to figure out whether a shared site makes sense, we can work through it with your data.

We take your telematics data, run the scenarios, and give you a clear recommendation on which charging mix best fits your fleet and how to get there.

Stefan, CEO @ Dodona

Read More