Deployment was never the hard part

The cheap money that built the charging industry has gone quiet. What comes next rewards a different kind of operator, and it puts fleets at the centre of the story.

The race to deploy left profitability behind

For about three years, building a charging network was mostly a question of speed. Capital was cheap, eager to fund deployment, and the brief from investors rarely changed. Put chargers in the ground, hit the number, and trust that demand will catch up. On paper, the money is still flowing. The appetite behind it has thinned, and the reason matters for anyone planning to rise in the next two years.

The force running the industry now is profitability. Many operators are not making money on the networks they have already built, and everyone can feel the shift. You can see it in who is buying whom. Networks are changing hands across the UK, and the language in every announcement is the same. More scale, a lower cost per site. That is a polite way of describing a route to profit that they could not reach on their own. These are not land grabs. They are the sound of capital running out of patience.

Demand is finally increasing, but not as a rescue

It is worth being clear about how we got here. There was a period of heavy investment built on the assumption that demand would come sooner or later, or at least sooner than it did. Then the last two years emptied the tank. Incentives dried up. The new administration in the United States turned policy back toward oil and rewrote the programmes that had underwritten build-outs. Europe felt the chill, too.

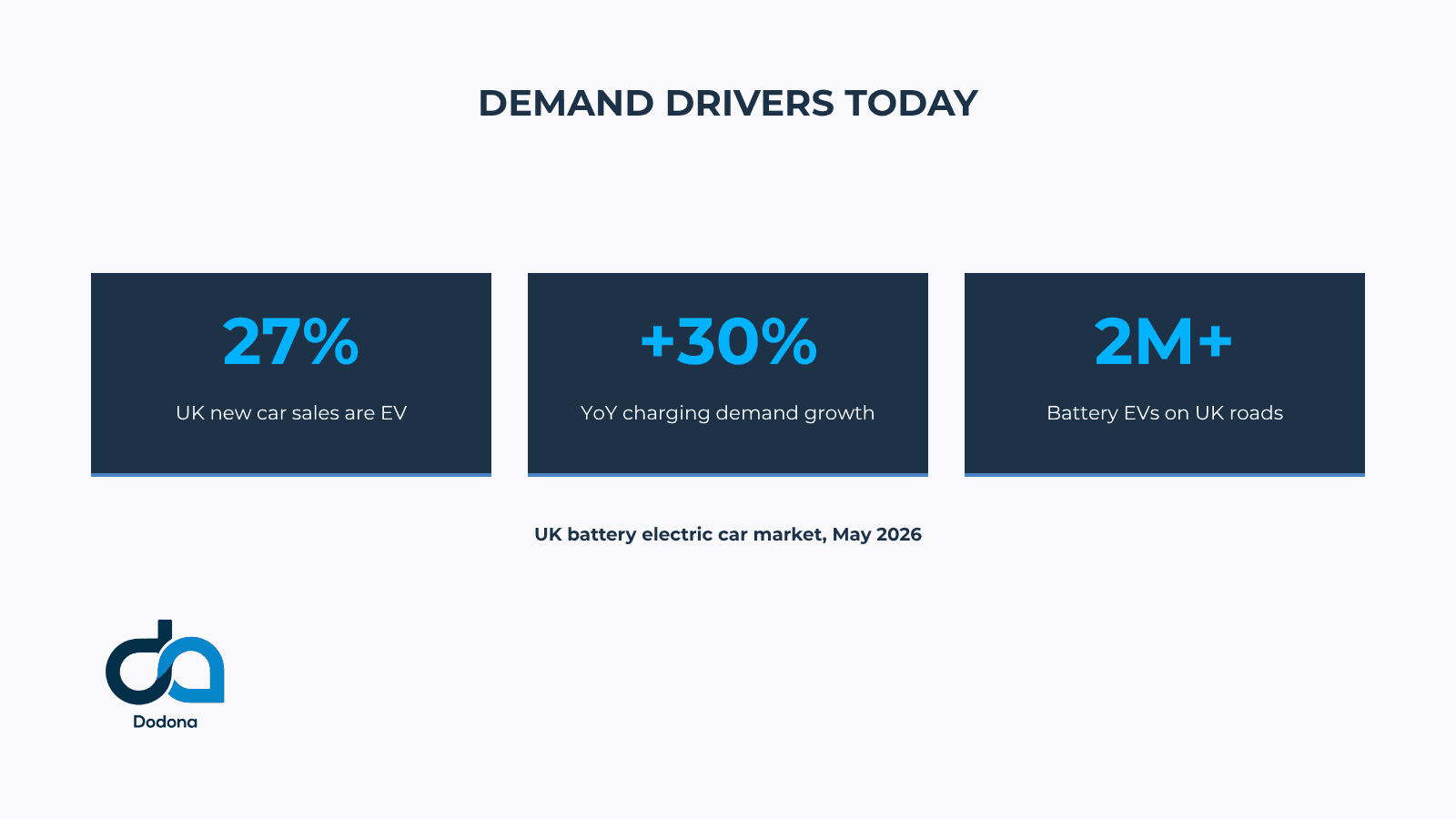

And then this spring, demand started to increase. Battery electric cars took around 27% of the UK new car market in May, up more than 30% on the year before, and March set a record. More than two million fully electric cars now drive the UK roads. The reasons are worth reading closely. Part of it is cheaper, more practical models, with mainstream brands leading rather than premium badges. The rest is fuel prices. Conflict in the Middle East has pushed petrol and diesel up, and a driver already weighing an electric next car now has one more reason to switch. That is a different buyer from the early adopter, and there are far more of them.

This is where operators get caught out. A surge in demand lifts the good sites and exposes the bad ones. It does nothing for a charger in the wrong place, and it does not repair a cost base that never made sense. More cars plugging in will not save a network someone built solely to hit a deployment target and overpaid for the site.

Why a charging network makes poor collateral

Which brings me to the money. Specifically, loan vs equity financing. A loan needs collateral, and a charging network makes poor collateral. Think about where the spend goes when you build a site. Only one part buys the hardware. The rest disappears into trenching, the grid connection, the civil works, the months of groundwork nobody ever sees. If the business fails, a lender can take the chargers. They cannot dig the cable back out of the ground, re-expose the concrete, or recoup the cost of the grid upgrade. That value stays with the landowner. Add a track record that gives a lender little basis for modelling when the loan gets repaid, and the debt comes off the table. That leaves equity, and today's equity investors ask a sharper question. Not how fast can you build, but when does the network start making money?

During the boom, almost nobody had to answer that. The deal was blunt. Here is the cash, put 300 chargers live by year-end. Quantity over quality. I sat in plenty of conversations where the whole target was a deployment number, and the honest reply, yes, but not at any price, rarely won the room. Operators bought sites in 2023 and 2024 at prices that only worked on demand that had yet to arrive. In hindsight, that was a bad trade. The operators who held their discipline and missed the deployment numbers back then look like the sensible ones now.

The industry has run this cycle before

We have watched this film before. When the railways and telecoms networks were first built, many early operators overspent, got overleveraged, and were later forced to sell their assets for pennies on the dollar. The businesses that did well were often the ones that bought those assets cheaply, out of the wreckage, and ran them with discipline. Charging is tracking the same path. Expect more networks to come to market this year, and the numbers are getting harder to hide.

So the operators who attract money now are the ones who already run as though money is scarce. The pattern repeats every time I look at a healthy network. They run more sites per person. They have not built a department for every problem, and they can tell you the economics of every site they operate. That discipline shows up twice. In how well they run what they have, and in how carefully they choose where the next charger goes. Those operators are still growing. They are still raising. That is not luck.

Fleets are the second engine, and most operators miss it

There is a second engine here, and it is the one most operators underplay. Fleets.

Electric vehicles are getting bigger and cheaper. Vans, heavier commercial vehicles, the workhorses cities run on, all of it is now within reach for buyers who order in volume. A large number of fleets are working through electrification right now. Three forces push them: net-zero commitments they set for themselves, city rules that make older diesels steadily more expensive to run, and major clients mandating net-zero from certain dates onwards.

Electrifying a fleet only works when three groups start working together, and most of them are used to ignoring each other. Vehicle makers and dealers are the first. Selling the van is no longer the whole job, because the fleet manager's next question is how to charge it. The maker or dealer who can answer that, or partner with someone who can, takes a share from those who hand over the keys and walk off. There is a real opening for dealers here right now. Fleet operators are the second. A fleet cannot simply order new vehicles and hope. They need a partner to help them work out which vehicles to switch, in what order, and how they will charge, grounded in how the fleet runs in practice rather than in a brochure. Charging providers are the third. The group spans public network operators and firms that build and run private depots. For an operator, a fleet is a heavy, predictable user. A deal with one guarantees energy offtake and lifts utilisation on sites that would otherwise sit idle between peaks.

Same vehicle count, completely different infrastructure

There is a catch, and it is the whole game. You cannot serve a fleet with a generic product. Say a depot has 24 vehicles to charge. If they trickle back one at a time through the evening and they need to be full by morning, you build one kind of site. If they all return at noon for a fast recharge and have to be ready again in 1 hour, you build something else entirely, with far more power and a much tighter energy plan. Same vehicle count, completely different infrastructure and economics. Read it wrong, and the fleet ends up unhappy as they have built the wrong thing.

The strategic point follows from that. Fleet vehicles cover far more miles than the average private car, so they pull a share of charging energy well above their share of vehicles on the road. An operator with no fleet-ready offer has quietly written off that demand. It is a decision, even when nobody set out to make it.

The work that Dodona was built to do

Connecting those three sides is the work done at Dodona, and we ground every decision in real demand rather than guesswork. For fleets, our Which, Where, When framework takes the questions in the order they arrive: which vehicles to transition first, where they will charge, and when to move.

The deploy-fast decade is over. The next one rewards whoever runs the tightest network and reads demand most clearly. The operators who also treat fleets as real customers, not an afterthought, will pull ahead. The money has already worked this out. The ones who make it through will be the operators who do the same before their next raise, not after.

One question is worth sitting with before that raise. Can you point at your network and say which sites make money and which lose it? And do you know where the next charger has to go to earn its place? That is the work we do at Dodona. If it is the question in front of you, let's talk.

Leading charge point operators trust our intelligent platform to optimize and scale their EV charging business with data-driven insights and AI automation.

Follow us:

Get in Touch

128 City Road, London, EC1V 2NX

370 Jay St, 7th Floor, New York, 11201

Dunajska cesta 5, 1000, Ljubljana

© Dodona Analytics Ltd